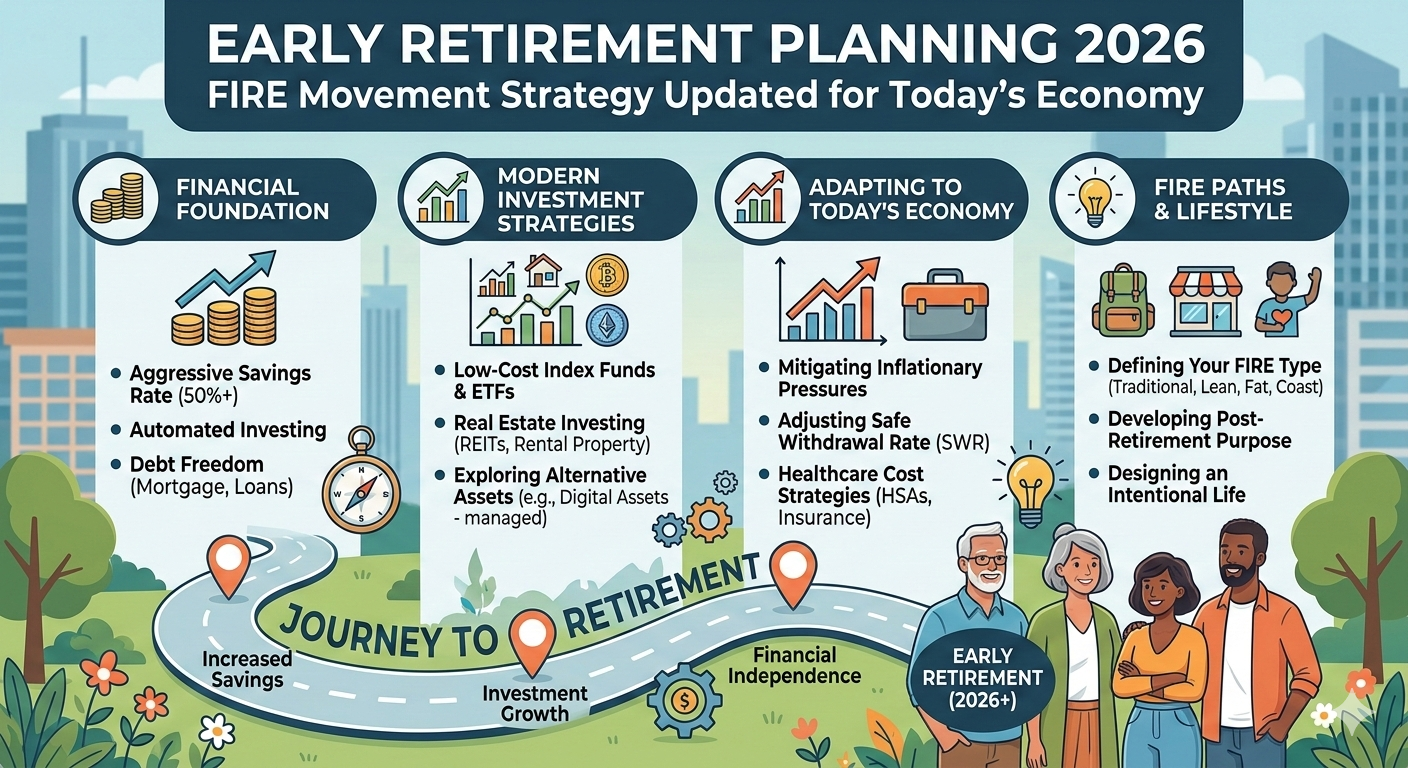

The FIRE movement strategy refers to a financial planning approach focused on achieving Financial Independence and Early Retirement (FIRE) through aggressive saving, disciplined investing, and controlled lifestyle expenses. The goal is to accumulate sufficient assets so investment returns can sustainably cover living costs without active employment.

Unlike traditional retirement models that target retirement after age 60, the FIRE movement strategy emphasizes retiring decades earlier by maximizing savings rates and building long-term passive income for retirement.

Financial independence occurs when investment income consistently exceeds annual expenses.

Core Principle Behind the FIRE Movement Strategy

The FIRE movement strategy operates on three financial foundations:

- High savings rate

- Long-term investment growth

- Expense optimization

Instead of relying solely on salary increases, individuals pursuing early retirement planning prioritize capital accumulation and compound growth.

According to historical market performance models, diversified investments have produced average long-term annual returns between 6%–8% after inflation adjustments.

Traditional Retirement vs FIRE Approach

| Factor | Traditional Retirement | FIRE Movement Strategy |

|---|---|---|

| Retirement Age | 60–67 | 35–55 |

| Savings Rate | 10–15% | 40–70% |

| Income Dependency | Employment | Investments |

| Lifestyle Adjustment | Late | Early |

| Financial Goal | Pension Security | Financial Independence |

The FIRE movement strategy shifts focus from lifetime employment toward asset-driven income.

Quick Insight

Early retirement planning under FIRE depends less on income level and more on savings behavior and investment consistency.

Why the FIRE Movement Strategy Is Growing Today

Economic uncertainty, rising living costs, and flexible digital income opportunities have accelerated interest in financial independence planning.

Modern workers increasingly seek:

- Control over working time

- Reduced dependence on employers

- Flexible career structures

- Long-term financial autonomy

The FIRE movement strategy aligns with these goals by prioritizing independence rather than delayed retirement.

Remote work expansion and scalable online income models further support passive income for retirement.

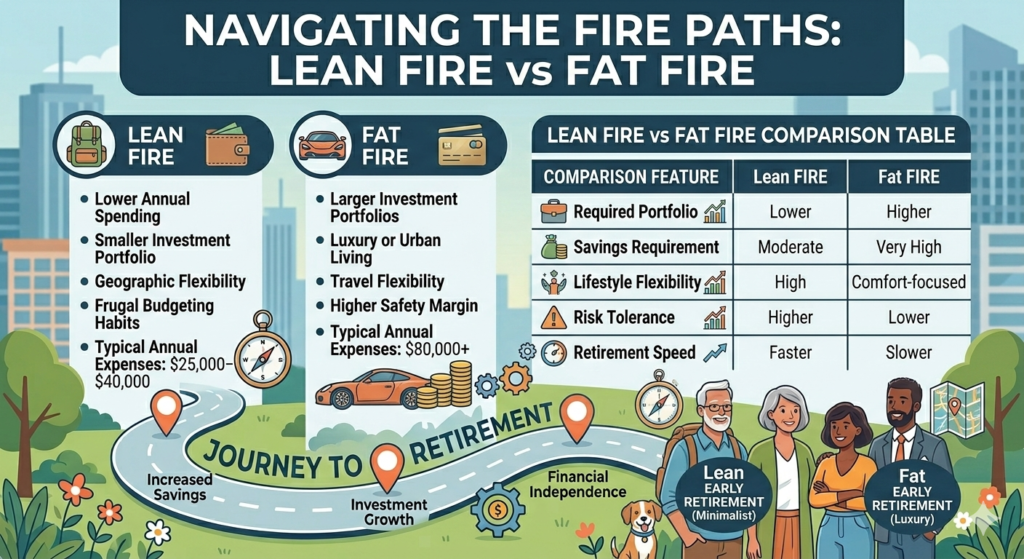

Types of FIRE: Lean FIRE vs Fat FIRE

Not all early retirement paths follow identical financial targets. Different lifestyle expectations create variations within the FIRE movement strategy.

Lean FIRE

Lean FIRE focuses on minimal living expenses and simplified lifestyles.

Characteristics include:

- Lower annual spending

- Smaller investment portfolio

- Geographic flexibility

- Frugal budgeting habits

Typical annual expenses: $25,000–$40,000

Fat FIRE

Fat FIRE supports higher lifestyle spending and financial comfort.

Characteristics include:

- Larger investment portfolios

- Luxury or urban living

- Travel flexibility

- Higher safety margin

Typical annual expenses: $80,000+

Lean FIRE vs Fat FIRE Comparison

| Feature | Lean FIRE | Fat FIRE |

|---|---|---|

| Required Portfolio | Lower | Higher |

| Savings Requirement | Moderate | Very High |

| Lifestyle Flexibility | High | Comfort-focused |

| Risk Tolerance | Higher | Lower |

| Retirement Speed | Faster | Slower |

Choosing between lean FIRE vs fat FIRE depends on spending expectations rather than income alone.

Takeaway

The FIRE movement strategy adapts to personal lifestyle goals rather than enforcing one retirement model.

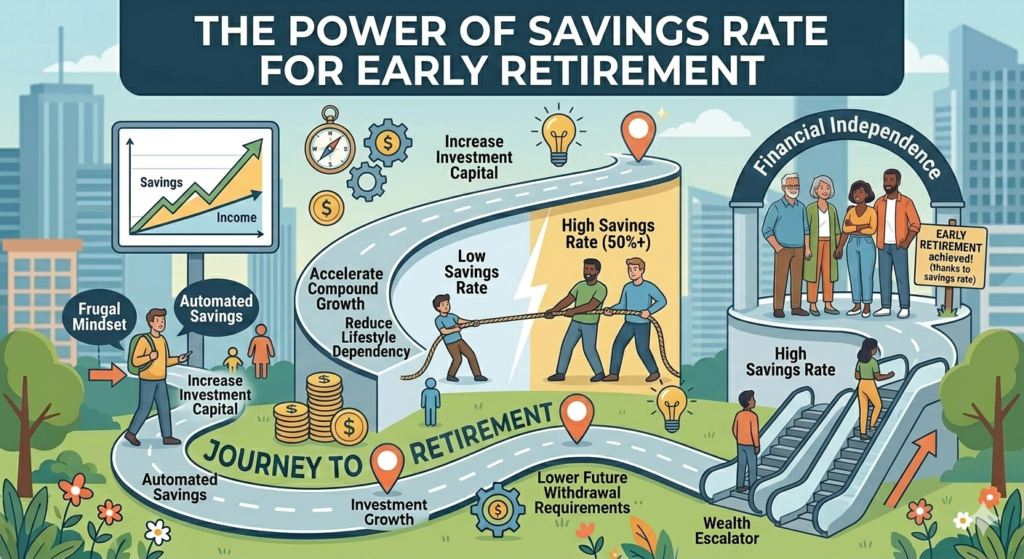

The Savings Rate for Early Retirement

Savings rate represents the most influential factor in early retirement planning.

The FIRE movement strategy prioritizes aggressive savings because investment capital determines retirement timeline.

Relationship Between Savings Rate and Retirement Time

| Savings Rate | Years to Financial Independence |

|---|---|

| 10% | 50+ Years |

| 25% | 32 Years |

| 40% | 22 Years |

| 50% | 17 Years |

| 65% | 10–12 Years |

Higher savings accelerate investment growth and reduce required working years.

Financial independence research consistently shows savings rate impacts retirement speed more than investment selection.

How to Increase Savings Rate Practically

Effective financial independence tips include:

- Automating investments

- Controlling lifestyle inflation

- Increasing income streams

- Reducing recurring expenses

- Optimizing housing costs

Small recurring expense reductions significantly improve long-term investment outcomes.

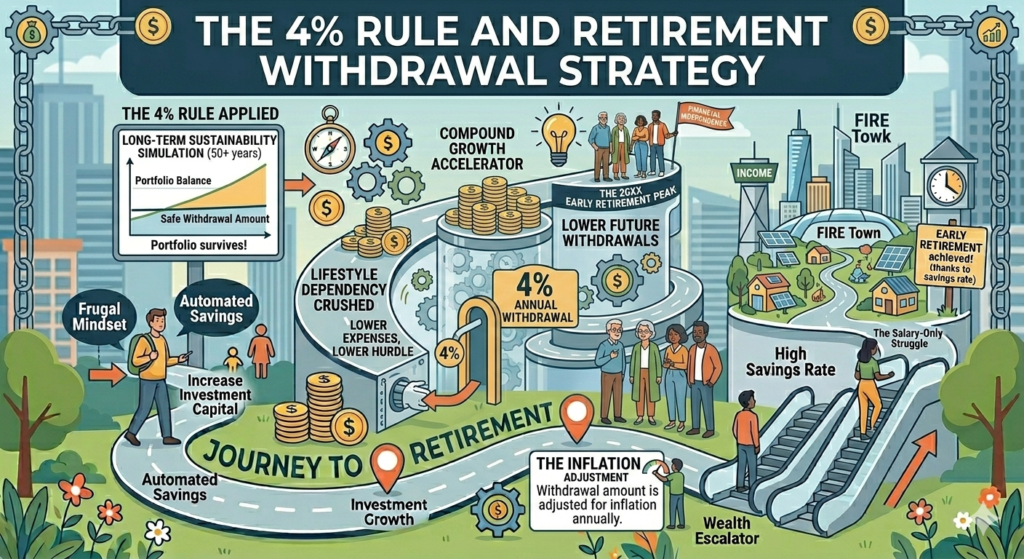

The 4% Rule and Retirement Withdrawal Strategy

A central component of the FIRE movement strategy involves determining safe withdrawal rates.

The widely referenced 4% rule suggests retirees can withdraw approximately 4% annually from investment portfolios without depleting funds over long periods.

Example:

| Portfolio Value | Annual Withdrawal |

|---|---|

| $500,000 | $20,000 |

| $1,000,000 | $40,000 |

| $1,500,000 | $60,000 |

This rule originates from historical market simulations analyzing diversified portfolios over multiple economic cycles.

Limitations in Today’s Economy

Modern early retirement planning adjusts withdrawal assumptions due to:

- Inflation volatility

- Healthcare expenses

- Market fluctuations

- Longevity increases

Many planners now model withdrawals between 3.5%–4% for additional safety.

Key Concept

The FIRE movement strategy depends on sustainable withdrawal rates rather than portfolio size alone.

Passive Income for Retirement Under FIRE

Passive income forms the operational engine of financial independence.

The FIRE movement strategy replaces salary income with recurring investment returns.

Major Passive Income Sources

Common retirement income channels include:

- Dividend-paying stocks

- Index fund investments

- Rental real estate

- Digital business assets

- Bond allocations

- Online intellectual property income

Diversification stabilizes retirement cash flow.

Passive vs Active Income in FIRE Planning

| Income Type | Effort Required | Scalability |

|---|---|---|

| Employment Income | Continuous | Limited |

| Freelancing | Moderate | Medium |

| Investment Income | Low | High |

| Digital Assets | Front-loaded | Very High |

Successful early retirees typically combine multiple passive income sources.

Using a Retire Early Calculator

A retire early calculator estimates required investment capital based on expenses and savings behavior.

Key inputs include:

- Annual expenses

- Savings rate

- Expected investment return

- Retirement age goal

- Inflation assumptions

Example calculation:

Annual expenses: $40,000

Required portfolio (4% rule):

≈ $1,000,000

Such tools help visualize progress toward financial independence milestones.

Variables That Affect Results

Retirement projections change significantly based on:

- Market performance

- Income growth

- Expense changes

- Investment consistency

Regular recalculation improves planning accuracy.

Investment Strategy Supporting FIRE

Investment allocation determines long-term success of the FIRE movement strategy.

Common Portfolio Allocation Model

| Asset Class | Allocation Range |

|---|---|

| Stock Index Funds | 60–80% |

| Bonds | 10–30% |

| Real Estate | 5–15% |

| Cash Reserves | 5–10% |

Diversified portfolios historically reduce long-term volatility risks.

Compound Growth Impact

Compound returns accelerate wealth accumulation over time.

Example:

Investing $1,500 monthly at 7% annual return:

| Years Invested | Portfolio Value |

|---|---|

| 10 Years | ~$260,000 |

| 20 Years | ~$780,000 |

| 30 Years | ~$1.8 Million |

Time remains the strongest advantage in early retirement planning.

Summary

- The FIRE movement strategy focuses on financial independence through savings and investing.

- Savings rate determines retirement timeline.

- Passive income replaces employment income.

- Withdrawal strategy ensures sustainability.

- Investment diversification protects long-term wealth.

Pros and Limitations of the FIRE Movement Strategy in Today’s Economy

The rapid adoption of the FIRE movement strategy reflects a structural shift in how individuals approach wealth building, career longevity, and retirement expectations. Traditional retirement models assumed employment until age 60–65. Modern economic uncertainty, digital income opportunities, and rising living costs have encouraged individuals to pursue early retirement planning through aggressive saving and investment systems.

The FIRE movement strategy focuses on accumulating sufficient assets so investment returns and passive income can sustainably replace employment income. However, while the framework offers measurable financial advantages, it also introduces practical risks that must be evaluated using updated economic conditions.

Advantages of the FIRE Movement Strategy

Early adopters increasingly view financial independence not as an endpoint but as a system that creates flexibility across work, lifestyle, and long-term planning decisions.

1. Financial Independence at an Earlier Age

The most significant benefit of the FIRE movement strategy is the ability to achieve independence decades before traditional retirement timelines.

Instead of relying on pension systems or late-career savings accumulation, individuals pursuing early retirement planning build investment portfolios capable of funding expenses through passive income for retirement.

This transition changes the role of employment entirely.

Key outcomes include:

- Freedom to work voluntarily rather than out of necessity

- Reduced dependence on economic cycles or layoffs

- Increased career experimentation

- Greater personal time control

- Ability to relocate or redesign lifestyle choices

Financial independence converts income generation from survival-driven activity into optional engagement.

According to long-term wealth accumulation models, individuals saving 50–70% of income may reach financial independence within 10–20 years depending on investment performance and spending discipline.

2. Strong Savings Discipline and Financial Awareness

A defining characteristic of successful early retirement planning is behavioral transformation.

Participants following the FIRE movement strategy typically develop structured financial habits that remain beneficial regardless of retirement goals.

These habits include:

- Detailed expense tracking

- Intentional consumption decisions

- Automated investing systems

- Debt minimization strategies

- Emergency fund prioritization

High savings behavior improves resilience during economic disruption such as inflation increases or employment instability.

| Financial Behavior | Traditional Model | FIRE-Oriented Model |

|---|---|---|

| Savings Rate | 10–15% | 40–70% |

| Budget Tracking | Occasional | Continuous |

| Investment Frequency | Irregular | Automated |

| Debt Dependency | Moderate | Minimal |

Higher savings rates reduce long-term financial vulnerability and accelerate asset accumulation.

3. Compound Growth Advantage

Compounding remains the mathematical foundation behind the FIRE movement strategy.

Early investing dramatically increases total wealth because returns generate additional returns over extended periods.

Example: Long-Term Compound Growth

| Starting Age | Monthly Investment | Value at Age 50 (7% Return) |

|---|---|---|

| Age 25 | $1,000 | ~$1.6 Million |

| Age 35 | $1,000 | ~$760,000 |

Beginning investments ten years earlier nearly doubles long-term portfolio value.

This demonstrates why early retirement planning emphasizes:

- Early market participation

- Consistent contributions

- Long investment horizons

- Low-cost diversified portfolios

(According to historical market performance data from diversified equity indices.)

4. Flexibility Instead of Permanent Retirement

Contrary to popular perception, most individuals applying the FIRE movement strategy do not permanently stop working.

Modern FIRE outcomes frequently include semi-retirement models, sometimes referred to as “financial independence lifestyles.”

Common post-independence activities include:

- Consulting or freelance work

- Digital entrepreneurship

- Remote professional services

- Creative or passion-based careers

- Education or mentoring roles

Financial independence expands choices rather than eliminating productivity.

Key Advantage

The FIRE movement strategy prioritizes time autonomy, not inactivity. Individuals gain control over when, how, and why they work.

5. Psychological Benefits of Financial Security

Economic research consistently links financial stress with reduced wellbeing and productivity.

Achieving independence through the FIRE movement strategy can reduce uncertainty related to:

- Job instability

- Economic recessions

- Income interruptions

- Unexpected life events

Financial buffers enable long-term decision-making instead of short-term survival planning.

However, psychological outcomes depend heavily on balanced implementation rather than extreme saving behaviors.

Also Read: Crypto Investment Strategy 2026: A Practical Guide to Digital Asset Planning for Everyday Investors

Challenges and Risks of Early Retirement Planning

While benefits are measurable, early retirement planning also introduces structural financial risks that must be addressed realistically.

1. Market Volatility Risk

Investment dependency represents the largest vulnerability within the FIRE movement strategy.

Retirement portfolios are exposed to economic cycles including:

- Stock market corrections

- Recession-driven asset declines

- Interest rate fluctuations

- Currency and inflation instability

A downturn occurring early in retirement—known as sequence-of-returns risk—can significantly reduce portfolio longevity.

Example scenario:

| Retirement Year | Market Return | Portfolio Impact |

|---|---|---|

| Year 1 | -20% | Major withdrawal stress |

| Year 2 | -10% | Recovery delay |

| Year 3 | +12% | Partial stabilization |

Early negative returns combined with withdrawals may permanently damage long-term sustainability.

Risk mitigation strategies often include diversified assets, flexible withdrawal rates, and contingency income sources.

2. Healthcare and Longevity Costs

Retiring decades earlier increases the number of years individuals must self-fund living and medical expenses.

Key considerations include:

- Private healthcare coverage

- Long-term insurance planning

- Emergency medical reserves

- Inflation-adjusted healthcare costs

In many economies, healthcare expenses rise faster than general inflation.

Longer life expectancy further increases planning complexity. Individuals retiring at age 40 may need portfolios lasting 45–50 years.

Early retirement planning must therefore incorporate conservative assumptions rather than optimistic projections.

3. Lifestyle Sustainability Challenges

Maintaining aggressive savings rates required by the FIRE movement strategy can create behavioral strain.

Common long-term challenges include:

- Burnout from extreme frugality

- Reduced social participation

- Family financial obligations

- Career opportunity trade-offs

Some participants experience motivation decline after reaching financial independence if lifestyle planning was overlooked.

Sustainable FIRE implementation typically balances saving efficiency with quality-of-life spending.

4. Inflation Impact on FIRE Plans

Inflation represents one of the most underestimated risks in early retirement planning.

Even moderate inflation significantly alters long-term expense requirements.

Inflation Illustration

| Annual Expense Today | Expense After 25 Years (3% Inflation) |

|---|---|

| $40,000 | ~$83,700 |

Failure to account for purchasing power erosion may cause retirement shortfalls despite seemingly adequate savings.

Modern FIRE models increasingly rely on:

- Inflation-adjusted withdrawal strategies

- Equity-heavy portfolios during early retirement

- Dynamic spending adjustments

5. Withdrawal Rate Uncertainty

Many FIRE plans historically relied on the “4% rule.” However, changing market conditions challenge fixed withdrawal assumptions.

Risks affecting withdrawal sustainability include:

- Lower bond yields

- Extended retirement duration

- Global economic instability

- Unexpected expense spikes

Flexible withdrawal frameworks now replace rigid models within updated FIRE movement strategy planning.

6. Identity and Purpose Transition

Employment provides structure, community interaction, and personal identity.

Early retirement may introduce non-financial challenges such as:

- Loss of professional identity

- Reduced social engagement

- Lack of structured routines

Successful early retirees often prepare lifestyle goals alongside financial independence objectives.

Risk Insight

The FIRE movement strategy succeeds when treated as an adaptable financial framework rather than a rigid mathematical formula. Sustainable early retirement planning requires diversification, behavioral balance, and continuous adjustment to economic conditions.

The modern FIRE movement strategy has evolved significantly in response to inflation trends, longer life expectancy, and changing employment structures. Earlier versions emphasized aggressive cost reduction alone, while updated early retirement planning combines income growth, diversified investments, and flexible retirement timelines.

Today, financial independence is increasingly achieved through adaptive models rather than a single rigid framework.

Understanding Modern FIRE Variations

Different lifestyle goals require different implementations of the FIRE movement strategy. Modern financial independence planning recognizes multiple FIRE categories designed to balance savings intensity with long-term sustainability.

Lean FIRE — Minimalist Early Retirement

Lean FIRE focuses on achieving early retirement with reduced living expenses and optimized consumption habits.

Individuals following this path typically prioritize:

- Low housing and transportation costs

- Minimal discretionary spending

- Geographic arbitrage (living in lower-cost regions)

- Simple lifestyle structures

Typical Lean FIRE Metrics

| Factor | Lean FIRE Range |

|---|---|

| Annual Expenses | $25,000–$40,000 |

| Savings Rate | 60–75% |

| Investment Target | $600K–$1M |

| Lifestyle Approach | Minimalist |

Advantages

- Faster path to financial independence

- Lower required investment portfolio

- Reduced dependence on employment income

Limitations

- Limited flexibility during emergencies

- Higher exposure to inflation increases

- Lifestyle sustainability challenges over decades

Lean FIRE works best for individuals comfortable maintaining disciplined spending habits throughout retirement.

Fat FIRE — Lifestyle-Oriented Financial Independence

Fat FIRE represents a higher-income implementation of the FIRE movement strategy, allowing early retirement without substantial lifestyle compromise.

Typical Fat FIRE Metrics

| Factor | Fat FIRE Range |

|---|---|

| Annual Expenses | $80,000–$150,000+ |

| Savings Rate | 30–50% |

| Required Portfolio | $2.5M–$5M+ |

| Lifestyle Style | Comfort-focused |

Fat FIRE supports:

- Travel flexibility

- Premium healthcare planning

- Family financial security

- Urban or high-cost living environments

This model generally requires higher earning capacity, entrepreneurship, or scalable investment income.

Barista FIRE — Hybrid Independence Model

Barista FIRE combines partial retirement with flexible or part-time employment.

Under this variation:

- Investments cover essential expenses

- Part-time income funds discretionary spending

- Withdrawal pressure on investments decreases

This approach reduces financial risk while maintaining psychological engagement through optional work.

Comparison Overview

| FIRE Type | Risk Level | Lifestyle Flexibility | Time to Achieve |

|---|---|---|---|

| Lean FIRE | Higher | Moderate | Faster |

| Barista FIRE | Moderate | High | Medium |

| Fat FIRE | Lower | Very High | Longer |

Savings Rate for Early Retirement

Savings rate remains the most influential variable within the FIRE movement strategy because it directly controls both investment growth and required retirement income.

Why Savings Rate Matters More Than Income

Income growth alone does not guarantee financial independence. Early retirement planning research consistently shows that savings behavior determines retirement timelines more than salary size.

Higher savings rates simultaneously:

- Increase investment capital

- Reduce lifestyle dependency

- Accelerate compound growth

- Lower future withdrawal requirements

Savings Rate vs Retirement Timeline

| Savings Rate | Estimated Years to Financial Independence |

|---|---|

| 10% | 50+ years |

| 25% | 30–32 years |

| 40% | 20–22 years |

| 60% | 12–15 years |

| 70% | ~10 years |

This mathematical relationship explains why the FIRE movement strategy prioritizes savings optimization rather than income expansion alone.

Practical Methods to Increase Savings Rate

Achieving sustainable early retirement planning requires systematic financial adjustments rather than extreme deprivation.

Expense Optimization Techniques

- Housing cost control (largest spending category)

- Transportation efficiency improvements

- Subscription and recurring expense audits

- Debt reduction strategies

- Tax-efficient investment allocation

Small recurring savings produce substantial long-term portfolio impact when compounded.

Income Expansion Approaches

Modern implementations of the FIRE movement strategy increasingly incorporate diversified income sources such as:

- Remote freelance work

- Digital entrepreneurship

- Consulting or skill monetization

- Investment reinvestment strategies

Increasing income while stabilizing expenses accelerates independence timelines significantly.

Passive Income for Retirement

Passive income represents the operational foundation of successful early retirement planning. Financial independence occurs when recurring investment income consistently exceeds annual living expenses.

Core Passive Income Categories

Investment-Based Income

Traditional passive income assets include:

- Dividend-paying equities

- Broad market index funds

- Government and corporate bonds

- Real Estate Investment Trusts (REITs)

Historically diversified portfolios have generated long-term growth capable of sustaining retirement withdrawals (based on long-term market performance data).

Digital and Scalable Income Streams

The modern FIRE movement strategy increasingly integrates digital income models capable of scaling without proportional time investment.

Examples include:

- Online educational products

- Digital publishing assets

- Automated online businesses

- Licensing and royalty-based income

These systems allow continued income generation even after workforce exit.

Withdrawal Strategies for Long-Term Sustainability

Portfolio withdrawal planning determines whether passive income for retirement remains sustainable across decades.

Updated Withdrawal Models

Modern FIRE planning increasingly applies flexible withdrawal frameworks:

- Dynamic withdrawal rates based on market performance

- Spending adjustments during downturns

- Cash reserve buffers

- Income diversification strategies

Rigid withdrawal assumptions are gradually being replaced by adaptive financial models suited to longer retirement periods.

Key Takeaway

A sustainable FIRE movement strategy combines diversified passive income, realistic savings targets, and flexible spending adjustments rather than relying solely on aggressive early accumulation.

Conclusion

The FIRE movement strategy continues to remain a viable framework for individuals seeking financial independence and long-term economic security. However, modern implementation differs significantly from early versions that relied primarily on extreme frugality.

Updated early retirement planning emphasizes:

- Sustainable savings rates instead of deprivation

- Diversified investment portfolios

- Flexible retirement timelines

- Multiple passive income for retirement sources

- Inflation-adjusted financial projections

Economic uncertainty, rising healthcare costs, and longer life expectancy require adaptive planning rather than rigid formulas. Individuals applying the FIRE movement strategy successfully treat financial independence as a continuous process rather than a fixed retirement event.

Achieving financial independence today depends on balancing savings discipline, income growth, and realistic lifestyle expectations. When implemented strategically, the FIRE movement strategy provides increased control over time, career decisions, and long-term financial stability.

Frequently Asked Questions (FAQs)

1. What is the FIRE movement strategy?

The FIRE movement strategy is a financial planning approach focused on achieving financial independence through high savings rates, disciplined investing, and passive income generation, allowing individuals to retire earlier than traditional retirement age.

2. What savings rate is required for early retirement planning?

Most early retirement planning models recommend saving 40% to 70% of income depending on retirement goals. Higher savings rates significantly reduce the number of working years needed to achieve financial independence.

3. What is the difference between Lean FIRE and Fat FIRE?

Lean FIRE involves retiring with lower annual expenses and minimalist living, while Fat FIRE supports early retirement with higher spending levels and lifestyle flexibility supported by a larger investment portfolio.

4. How much money is needed to follow the FIRE movement strategy?

Required savings depend on annual expenses. A commonly used guideline estimates retirement assets at 25–30 times yearly expenses, adjusted for inflation and market conditions.

5. Is passive income necessary for early retirement?

Yes. Passive income for retirement—such as dividends, index funds, rental income, or digital assets—is essential because it replaces employment income and sustains long-term financial independence.

6. What risks are associated with the FIRE movement strategy?

Key risks include:

- Market volatility

- Inflation impact

- Healthcare expenses

- Longevity risk

- Withdrawal rate miscalculations

Proper diversification and flexible spending strategies reduce these risks.

7. Can average-income earners achieve financial independence?

Yes. The FIRE movement strategy is primarily influenced by savings behavior and investment consistency rather than income level alone. Increasing savings rate and maintaining long-term investment discipline significantly improve outcomes.

Disclaimer:

The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. The author is not a licensed financial advisor. Readers should conduct their own research and consult a qualified financial professional before making any financial or investment decisions.