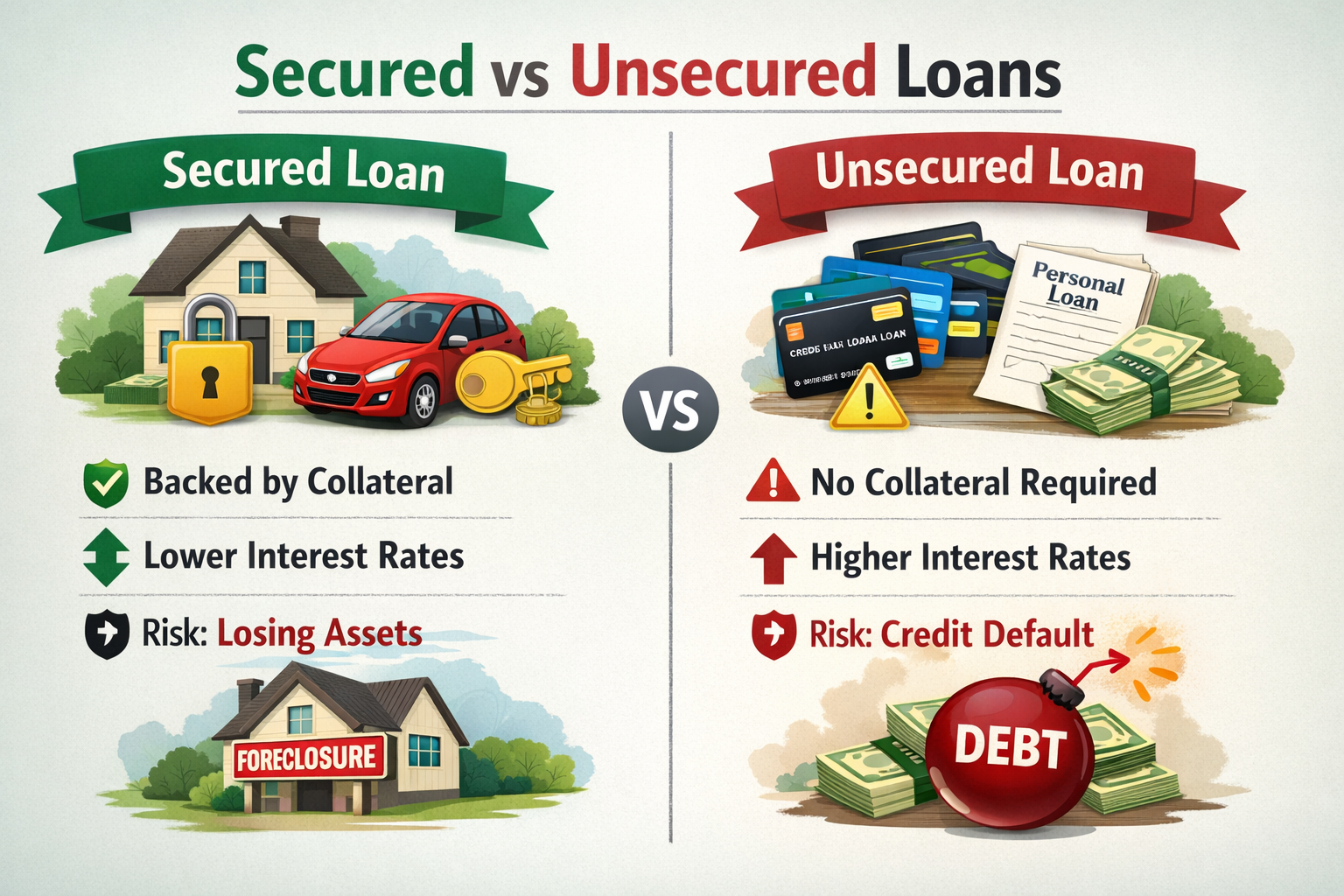

A secured loan is a type of borrowing that requires the borrower to provide an asset as collateral. Collateral is something valuable that the lender can legally take if the borrower fails to repay the loan. Common examples include a house, car, or savings account.

In secured vs unsecured loans, the presence of collateral is the defining feature. Because the lender has a claim over an asset, the financial risk for the lender is lower. As a result, secured loans often offer:

- Lower interest rates

- Higher borrowing limits

- Longer repayment periods

If a borrower defaults, the lender can seize and sell the collateral to recover the unpaid balance. This legal right is typically defined in the loan agreement and supported by lending laws.

What Is an Unsecured Loan?

An unsecured loan does not require collateral. Approval is based primarily on the borrower’s creditworthiness, income, and financial history. The lender relies on the borrower’s promise to repay rather than an asset.

When comparing secured vs unsecured loans, unsecured borrowing shifts more risk to the lender. Because there is no collateral to recover losses, lenders compensate by charging higher interest rates.

Unsecured loans typically have:

- Higher interest rates

- Lower borrowing limits

- Stricter credit score requirements

- Shorter repayment terms

If a borrower defaults on an unsecured loan, the lender cannot immediately seize property. However, they may pursue collection efforts, legal action, or wage garnishment depending on jurisdiction and contract terms.

Key Structural Difference Between the Two

The core difference in secured vs unsecured loans is risk allocation.

| Factor | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral Required | Yes | No |

| Lender Risk | Lower | Higher |

| Interest Rates | Typically lower | Typically higher |

| Asset Seizure Risk | Yes | No direct seizure |

| Credit Requirement | Moderate to strict | Usually strict |

In simple terms:

- Secured loans protect the lender with an asset.

- Unsecured loans rely on borrower credit strength.

- In a high-interest economy, this structural difference becomes more significant because borrowing costs rise across the market.

According to lending standards influenced by institutions such as the Federal Reserve, rising benchmark rates increase overall borrowing costs, but unsecured products tend to experience sharper rate increases due to higher perceived risk.

Summary

Secured loans require collateral and usually offer lower rates but carry asset seizure risk. Unsecured loans do not require collateral but typically charge higher interest due to increased lender risk.

Key Takeaways

- Collateral is the main difference between secured and unsecured borrowing.

- Lender risk determines interest rates.

- Secured loans may be cheaper but risk asset loss.

- Unsecured loans protect assets but cost more.

- Economic conditions amplify these differences.

Secured vs Unsecured Loans: Core Differences

Understanding the structural gap in secured vs unsecured loans is essential before deciding which option fits your financial situation. The difference between secured and unsecured loan products goes beyond collateral — it affects approval, cost, borrowing power, and long-term risk exposure.

Collateral Requirements

The most important difference in secured vs unsecured loans is whether collateral is required.

- Secured loans require an asset such as property, a vehicle, or savings.

- Unsecured loans require no asset pledge.

Collateral reduces lender risk. If the borrower fails to repay, the lender has legal rights to claim the asset. In contrast, unsecured borrowing depends entirely on creditworthiness and legal recovery methods.

Why This Matters in a High-Interest Economy

When rates rise, lenders become more risk-sensitive. Secured lending remains relatively stable because assets reduce default losses. Unsecured products may tighten approval standards.

Approval Criteria

Approval standards differ significantly in secured vs unsecured loans.

Secured Loan Approval Factors

- Asset value (Loan-to-Value ratio)

- Income stability

- Credit profile

- Debt-to-income ratio

Unsecured Loan Approval Factors

- Credit score

- Income level

- Employment consistency

- Existing debt obligations

Because lenders lack collateral protection in unsecured loans, they usually require stronger credit profiles. In contrast, secured products may approve borrowers with moderate credit if collateral value is sufficient.

According to consumer lending oversight standards referenced by the Consumer Financial Protection Bureau, lenders evaluate borrower repayment capacity carefully when collateral is absent.

Interest Rate Structure

Interest pricing reflects risk. In secured vs unsecured loans, this is one of the clearest differences.

| Factor | Secured Loan | Unsecured Loan |

|---|---|---|

| Risk to Lender | Lower | Higher |

| Interest Rate Level | Generally lower | Generally higher |

| Rate Sensitivity | Moderate | High |

| Variable Rate Risk | Present in some products | Common in personal loans |

Unsecured personal loan interest rates are usually higher because lenders cannot recover losses through asset seizure. In a rising-rate environment, unsecured rates often increase faster than secured rates.

Loan Amount Limits

Borrowing capacity also differs in secured vs unsecured loans.

- Secured loans often allow larger amounts because lending is tied to asset value.

- Unsecured loans typically cap borrowing limits based on income and credit score.

For example:

- Mortgage loans can finance large property values.

- Unsecured personal loans may be limited to smaller amounts relative to income.

This structural difference affects risk exposure during economic tightening cycles.

Also Read: Student Loan Forgiveness

Repayment Terms

Repayment structures vary between secured vs unsecured loans.

Secured Loans

- Longer repayment terms

- Fixed or variable options

- Lower monthly payments (spread over time)

Unsecured Loans

- Shorter repayment periods

- Higher monthly payments due to higher rates

- Limited flexibility in restructuring

In a high-interest economy influenced by rate policy from institutions like the Federal Reserve, shorter-term unsecured loans may become more expensive month-to-month compared to long-term secured borrowing.

Core Comparison

| Dimension | Secured | Unsecured |

|---|---|---|

| Collateral | Required | Not required |

| Approval Flexibility | Moderate | Strict |

| Interest Cost | Lower | Higher |

| Risk of Asset Loss | Yes | No |

| Default Recovery | Asset seizure | Legal action & collections |

Summary

The core differences in secured vs unsecured loans involve collateral, pricing, approval standards, and risk distribution. Secured loans lower lender risk through asset backing, while unsecured loans increase borrower cost due to higher interest rates and stricter credit requirements.

Key Takeaways

- Collateral defines the structure.

- Interest rates reflect risk.

- Secured loans support larger borrowing.

- Unsecured loans require stronger credit.

- High interest rates widen cost differences.

Secured vs Unsecured Loans and Interest Rates in a High-Interest Economy

Interest rates are the most sensitive factor in secured vs unsecured loans, especially during periods of monetary tightening. In a high-interest economy, borrowing costs rise across all loan types. However, the impact is not equal.

Understanding how rate changes affect secured vs unsecured loans helps borrowers evaluate safety, affordability, and long-term risk.

Why Unsecured Personal Loan Interest Rates Are Higher

In secured vs unsecured loans, unsecured products almost always carry higher rates. The reason is risk pricing.

Lenders calculate interest based on:

- Probability of default

- Loss recovery potential

- Borrower credit strength

- Economic outlook

With secured loans, the lender can recover losses through collateral. With unsecured loans, recovery depends on legal collection processes, which may not fully compensate losses. Because of this uncertainty, lenders charge higher interest.

In a high-interest economy, unsecured personal loan interest rates often rise faster because:

- Credit risk increases during economic stress

- Delinquencies tend to rise when inflation pressures household budgets

- Lenders tighten underwriting standards

As documented by monetary policy frameworks used by the Federal Reserve, benchmark rate increases influence consumer lending costs across the financial system.

How Central Bank Rate Hikes Affect Borrowers

When central banks raise policy rates to control inflation, lending costs increase. This affects secured vs unsecured loans differently.

Impact on Secured Loans

- Mortgage and auto loan rates increase gradually

- Long-term loans may still offer relatively lower rates due to asset backing

- Fixed-rate borrowers are protected from future hikes

Impact on Unsecured Loans

- Personal loan APRs adjust upward quickly

- Variable-rate products become more expensive

- Credit card rates often rise immediately

The difference between secured and unsecured loan pricing becomes more visible during rate hikes because unsecured lenders face higher default probability without collateral protection.

Rate Sensitivity Comparison Table

| Factor | Secured Loan | Unsecured Loan |

|---|---|---|

| Base Interest Rate | Lower | Higher |

| Reaction to Rate Hikes | Moderate | Rapid |

| Default Risk Premium | Lower | Higher |

| Monthly Payment Volatility | Lower (if fixed) | Higher |

| Long-Term Cost Risk | Asset-linked | Credit-risk linked |

This table shows how secured vs unsecured loans respond differently when borrowing conditions tighten.

Risk Amplification in a High-Interest Economy

In a high-rate environment:

- Monthly payments increase

- Debt servicing ratios rise

- Household financial stress grows

For secured loans, the main risk is asset loss if payments fail.

For unsecured loans, the risk is higher interest burden and faster accumulation of total repayment cost.

Institutions such as the International Monetary Fund have noted that elevated interest rates increase household debt vulnerability globally, particularly in unsecured consumer credit markets.

Safety Perspective Under Rising Rates

When evaluating secured vs unsecured loans during high interest periods:

- Secured loans may offer lower borrowing costs but carry asset seizure risk.

- Unsecured loans protect assets but can become expensive quickly.

- Rate volatility affects unsecured products more strongly.

Safety depends on income stability, risk tolerance, and asset protection priorities.

Summary

In a high-interest economy, unsecured loans typically experience faster rate increases and higher total borrowing costs. Secured loans often maintain relatively lower rates due to collateral protection but expose borrowers to asset loss if default occurs.

Key Takeaways

- Interest rates reflect lender risk.

- Unsecured personal loan interest rates are usually higher.

- Rate hikes widen the cost gap.

- Secured loans reduce interest burden but increase asset risk.

- Economic tightening amplifies borrowing differences.

Collateral Loan Risks Borrowers Must Understand

When comparing secured vs unsecured loans, collateral introduces a different category of risk. While secured borrowing may offer lower interest rates, it exposes the borrower to asset-related dangers that do not exist in unsecured credit.

Understanding collateral loan risks is critical in a high-interest economy where repayment pressure increases.

Asset Seizure Risk

The most serious risk in secured vs unsecured loans occurs when a borrower defaults on a secured loan.

If payments stop:

- The lender can repossess the pledged asset.

- The asset may be sold to recover the outstanding balance.

- The borrower may still owe money if the sale does not cover the debt.

Examples include:

- Home foreclosure in mortgage default.

- Vehicle repossession in auto loan default.

- Asset liquidation in secured business lending.

This direct seizure risk does not apply in unsecured borrowing. However, unsecured lenders may still pursue legal action.

Property Depreciation Risk

Collateral loan risks extend beyond default.

In secured vs unsecured loans, the value of collateral matters. If asset prices decline:

- Loan-to-Value (LTV) ratios increase.

- Borrowers may owe more than the asset is worth.

- Refinancing becomes difficult.

For example, in a housing downturn:

- A homeowner may face negative equity.

- Selling the property may not clear the debt.

High-interest environments sometimes slow asset markets, increasing this risk.

Overleveraging Risk

Secured borrowing can encourage larger loan amounts because lenders feel protected by collateral.

In secured vs unsecured loans, secured products often allow higher borrowing limits. This creates overleveraging risk:

- Borrowers may take larger loans than necessary.

- Rising interest rates increase repayment pressure.

- Debt servicing consumes a larger share of income.

Overleveraging becomes especially dangerous during economic slowdowns when income stability weakens.

According to global financial stability assessments referenced by the World Bank, high household leverage increases vulnerability during rate tightening cycles.

Emotional and Financial Impact

Collateral loss is not just financial — it can be life-altering.

In secured vs unsecured loans:

- Secured default may result in losing a home or vehicle.

- Unsecured default may damage credit but does not directly remove essential assets.

The emotional stress of asset loss often exceeds the financial cost alone. This factor plays a significant role in evaluating which loan type is safer.

Collateral Risk Comparison

| Risk Type | Secured Loan | Unsecured Loan |

|---|---|---|

| Asset Seizure | Yes | No |

| Depreciation Impact | Yes | No |

| Overleveraging Risk | Higher (larger loans) | Moderate |

| Emotional Stress from Default | High | Moderate |

| Direct Property Loss | Possible | Not direct |

This comparison highlights how secured vs unsecured loans distribute risk differently between borrower and lender.

Summary

Collateral loan risks include asset seizure, depreciation exposure, and overleveraging. While secured loans may lower interest costs, they increase the potential for property loss if repayment fails.

Key Takeaways

- Collateral reduces lender risk but increases borrower exposure.

- Asset value fluctuations affect secured borrowers.

- High interest rates increase default pressure.

- Losing essential assets can create long-term financial instability.

- Risk evaluation should include both financial and personal factors.

Loan Default Consequences in Secured vs Unsecured Loans

Default is the most critical risk factor when evaluating secured vs unsecured loans. While both loan types carry legal and financial consequences, the recovery process and impact on the borrower differ significantly.

Understanding loan default consequences is essential in a high-interest economy where repayment pressure increases.

Default Process for Secured Loans

In secured vs unsecured loans, secured default triggers asset-based recovery.

When a borrower misses payments:

- The lender issues delinquency notices.

- Late fees and penalty interest may apply.

- After prolonged nonpayment, the lender initiates repossession or foreclosure.

- The asset is sold to recover outstanding debt.

If the sale does not fully cover the loan balance, the borrower may still owe the remaining amount, known as a deficiency balance.

Common secured default outcomes include:

- Home foreclosure

- Vehicle repossession

- Seizure of pledged savings or business assets

Because collateral is legally tied to the loan agreement, recovery is typically faster and more direct.

Default Process for Unsecured Loans

In secured vs unsecured loans, unsecured default follows a different path.

If payments stop:

- The account becomes delinquent.

- The lender sends collection notices.

- The debt may be transferred to a collection agency.

- Legal action may be pursued.

Unlike secured loans, there is no immediate asset seizure. However, court judgments can lead to:

- Wage garnishment

- Bank account levies

- Property liens (depending on jurisdiction)

Although unsecured default does not automatically remove property, legal consequences can still be severe.

Legal Actions and Collections

The legal pathway differs in secured vs unsecured loans.

| Factor | Secured Loan | Unsecured Loan |

|---|---|---|

| Immediate Asset Seizure | Yes (after process) | No |

| Court Involvement Required | Often not for repossession | Usually required |

| Wage Garnishment | Possible after deficiency | Possible after judgment |

| Collection Agencies | Less common | Very common |

| Public Record Impact | Foreclosure record | Civil judgment record |

Consumer protection guidelines outlined by the Consumer Financial Protection Bureau describe borrower rights during collections and legal enforcement.

Credit Score Damage Timeline

In secured vs unsecured loans, both types severely affect credit scores if default occurs.

Typical credit impact pattern:

- 30 days late: Significant score drop

- 60–90 days late: Further damage

- Charge-off or foreclosure: Major negative mark

- Collection account: Long-term credit impact

Negative marks can remain on credit reports for several years, affecting:

- Future loan approvals

- Insurance premiums

- Rental applications

Although asset loss is unique to secured loans, credit damage is common to both loan types.

Financial Impact Comparison

| Consequence | Secured Loan Default | Unsecured Loan Default |

|---|---|---|

| Loss of Property | Likely | Not direct |

| Credit Score Damage | Severe | Severe |

| Legal Risk | Moderate | High (court action) |

| Emotional Impact | High (asset loss) | Moderate |

| Long-Term Financial Recovery | Slower | Moderate |

This comparison shows how secured vs unsecured loans distribute default consequences differently between asset risk and legal risk.

Summary

Default consequences in secured loans include asset seizure and possible deficiency balances. Unsecured default typically results in collections and legal action. Both loan types severely damage credit, but secured borrowing carries direct property loss risk.

Key Takeaways

- Secured default can result in losing pledged assets.

- Unsecured default may lead to lawsuits and wage garnishment.

- Both types cause serious credit damage.

- High-interest environments increase default probability.

- Understanding consequences helps assess which loan type is safer.

Secured Loan Examples and When They Make Sense

To fully understand secured vs unsecured loans, it is important to examine real-world secured loan examples. Secured loans are commonly used for large purchases or long-term financing needs because they allow lower interest rates in exchange for collateral.

In a high-interest economy, secured loans may appear more affordable monthly, but they still carry asset risk.

Mortgage Loans

A mortgage is one of the most common secured loan examples.

- The property being purchased serves as collateral.

- If the borrower defaults, foreclosure may occur.

- Interest rates are generally lower than unsecured credit.

In secured vs unsecured loans, mortgages represent long-term borrowing backed by real estate. Because property typically holds significant value, lenders offer extended repayment periods.

However, rising interest rates increase monthly payments for adjustable-rate mortgages, increasing foreclosure risk if income is unstable.

Auto Loans

Auto loans are another typical secured product.

- The vehicle acts as collateral.

- Repossession may occur after prolonged nonpayment.

- Loan terms are usually shorter than mortgages.

When comparing secured vs unsecured loans, auto loans illustrate how lenders reduce risk by tying financing directly to the asset being purchased.

Vehicle depreciation is a key risk factor. If the car loses value faster than the loan balance declines, borrowers may owe more than the car’s market value.

Secured Business Loans

Businesses often use secured financing to obtain larger capital amounts.

- Equipment, inventory, or property may serve as collateral.

- Rates are typically lower than unsecured business credit.

- Approval may be easier if assets are strong.

In secured vs unsecured loans, business lending demonstrates how collateral improves borrowing capacity. However, economic slowdowns can reduce business revenue, increasing asset seizure risk.

Global financial institutions such as the International Monetary Fund have noted that rising interest environments can strain leveraged businesses.

Home Equity Loans

Home equity loans allow homeowners to borrow against the equity in their property.

- The home serves as collateral.

- Interest rates are usually lower than unsecured personal loans.

- Borrowers risk foreclosure if repayment fails.

In secured vs unsecured loans, home equity borrowing can consolidate higher-interest debt. However, converting unsecured debt into secured debt increases asset exposure.

When Secured Loans Make Sense

Secured borrowing may be appropriate when:

- The borrower needs a large loan amount.

- Income is stable and predictable.

- Interest rate savings are substantial.

- The asset being pledged is not essential for survival.

However, borrowers must evaluate risk carefully. Lower rates do not eliminate the possibility of default under financial stress.

Secured Loan Risk

| Example | Collateral | Main Benefit | Main Risk |

|---|---|---|---|

| Mortgage | Home | Lower long-term rate | Foreclosure |

| Auto Loan | Vehicle | Easier approval | Repossession |

| Business Loan | Business assets | Larger capital access | Asset liquidation |

| Home Equity Loan | Home equity | Debt consolidation | Property loss |

This breakdown shows how secured vs unsecured loans differ in practical application.

Summary

Secured loan examples include mortgages, auto loans, business loans, and home equity loans. They offer lower rates and higher limits but expose borrowers to asset seizure if default occurs.

Key Takeaways

- Secured loans are common for large purchases.

- Collateral allows lower interest rates.

- Asset depreciation increases financial risk.

- Converting unsecured debt into secured debt raises exposure.

- Stability of income is critical before pledging assets.

Which Loan Type Is Better in a High-Interest Economy?

Choosing between secured vs unsecured loans during a high-interest economy depends on risk tolerance, income stability, and asset protection priorities. There is no universal answer. The safer option varies by financial situation.

Rising interest rates increase borrowing costs across all credit types, but risk exposure differs significantly between secured vs unsecured loans.

Risk Tolerance Analysis

Risk tolerance plays a central role in deciding between secured vs unsecured loans.

Borrowers with low risk tolerance may prefer unsecured loans because:

- No direct asset seizure occurs.

- Essential property is protected.

- Default does not automatically result in losing a home or vehicle.

Borrowers with higher risk tolerance may choose secured loans to:

- Access lower interest rates.

- Reduce monthly payment burden.

- Borrow larger amounts.

However, lower rates should not overshadow the risk of losing pledged assets.

Income Stability Consideration

In a high-interest environment, repayment pressure increases. When comparing secured vs unsecured loans, income stability becomes critical.

If income is:

- Stable and predictable → Secured loans may be manageable.

- Variable or uncertain → Unsecured loans may reduce asset loss risk.

Interest rate increases, often influenced by institutions like the Federal Reserve, can raise monthly obligations, making stable income essential for secured borrowing.

Asset Protection Strategy

Asset protection is one of the most important factors in secured vs unsecured loans.

Consider:

- Is the asset essential (primary home, work vehicle)?

- Would losing it create long-term hardship?

- Is there emergency savings available?

Secured borrowing ties financial obligations directly to property. In contrast, unsecured borrowing isolates debt risk from physical assets.

Summary

In a high-interest economy, secured loans may reduce borrowing costs but increase asset loss risk. Unsecured loans protect property but typically carry higher interest rates. The better choice depends on income stability, asset importance, and risk tolerance.

Key Takeaways

- There is no universally safer loan type.

- Secured loans lower interest but raise asset exposure.

- Unsecured loans cost more but protect property.

- Stable income supports secured borrowing.

- Risk tolerance determines the safer option.

Pros and Cons of Secured vs Unsecured Loans

Evaluating secured vs unsecured loans requires weighing advantages and disadvantages carefully. Each loan type shifts risk differently between the borrower and lender. In a high-interest economy, these trade-offs become more significant.

Advantages of Secured Loans

Secured loans provide structural benefits because collateral reduces lender risk.

Key Advantages:

- Lower interest rates compared to unsecured products

- Higher borrowing limits

- Longer repayment periods

- Potentially easier approval with moderate credit

In secured vs unsecured loans, secured borrowing often reduces total interest cost over time, especially for large loan amounts.

Disadvantages of Secured Loans

Despite lower interest costs, secured loans carry serious risks.

Key Disadvantages:

- Risk of asset seizure

- Foreclosure or repossession consequences

- Possible deficiency balance after asset sale

- Emotional stress from property loss

In secured vs unsecured loans, secured borrowing exposes essential assets to financial distress if income declines or rates rise.

Advantages of Unsecured Loans

Unsecured loans prioritize asset protection.

Key Advantages:

- No collateral required

- No direct property loss upon default

- Faster approval process in many cases

- Suitable for short-term borrowing needs

In secured vs unsecured loans, unsecured products provide flexibility and reduce long-term asset exposure.

Disadvantages of Unsecured Loans

Higher lender risk results in higher borrower cost.

Key Disadvantages:

- Higher interest rates

- Lower borrowing limits

- Stricter credit requirements

- Greater monthly payment burden

Unsecured personal loan interest rates typically rise faster in tightening economic conditions influenced by global monetary policy trends observed by institutions like the World Bank.

Pros and Cons Comparison Table

| Category | Secured Loan | Unsecured Loan |

|---|---|---|

| Interest Cost | Lower | Higher |

| Asset Risk | High | None (direct) |

| Approval Flexibility | Moderate | Strict |

| Borrowing Capacity | Higher | Lower |

| Default Outcome | Asset loss | Legal collection |

| Rate Sensitivity | Moderate | High |

This structured comparison clarifies how secured vs unsecured loans balance cost and risk differently.

Summary

Secured loans offer lower interest rates and higher limits but expose borrowers to asset seizure. Unsecured loans protect assets but usually carry higher borrowing costs and stricter approval requirements.

Key Takeaways

- Secured loans trade asset risk for lower rates.

- Unsecured loans trade higher cost for asset safety.

- Economic tightening increases unsecured borrowing costs faster.

- The safer option depends on financial stability and asset importance

Common Mistakes Borrowers Make When Choosing Between Secured vs Unsecured Loans

When comparing secured vs unsecured loans, many borrowers focus only on interest rates and overlook long-term risk exposure. In a high-interest economy, these mistakes can significantly increase financial vulnerability.

Understanding common errors helps borrowers avoid unnecessary default risk and long-term financial damage.

Choosing Based Only on Interest Rate

A lower rate does not automatically mean a safer loan.

In secured vs unsecured loans:

- Secured loans may offer lower APR.

- However, they expose valuable assets to seizure.

Borrowers sometimes ignore asset risk and choose secured borrowing solely for cost savings. This can be dangerous if income becomes unstable.

Ignoring Collateral Loan Risks

Collateral loan risks are often underestimated.

Common oversight:

- Not evaluating whether the pledged asset is essential.

- Not considering potential asset depreciation.

- Assuming property values will always remain stable.

In secured vs unsecured loans, failing to assess collateral risk can lead to foreclosure or repossession during economic downturns.

Underestimating Loan Default Consequences

Some borrowers assume unsecured default has minor consequences.

In reality:

- Credit scores drop sharply.

- Collection agencies may pursue repayment.

- Court judgments can lead to wage garnishment.

Both secured vs unsecured loans carry serious default consequences, though the nature of the risk differs.

Overleveraging Because Approval Is Available

Secured borrowing often allows larger loan amounts.

Mistake:

- Borrowing the maximum amount offered.

- Not stress-testing repayment ability under higher rates.

In a high-interest economy, rising monthly payments can strain budgets quickly.

Financial stability reports from institutions such as the International Monetary Fund highlight how household overleveraging increases default risk during monetary tightening.

Not Considering Rate Volatility

Many unsecured loans and some secured loans have variable rates.

Mistake:

- Ignoring how rate hikes affect monthly payments.

- Assuming current rates will remain stable.

When central banks adjust policy rates, borrowing costs can increase rapidly, affecting affordability.

Converting Unsecured Debt Into Secured Debt Without Strategy

Some borrowers use home equity loans to pay off unsecured debt.

Risk:

- Turning unsecured debt into secured debt increases asset exposure.

- Default consequences become more severe.

In secured vs unsecured loans, shifting debt types changes risk distribution significantly.

| Mistake | Potential Outcome |

|---|---|

| Focusing only on interest rate | Asset loss risk ignored |

| Ignoring collateral risk | Foreclosure or repossession |

| Underestimating default consequences | Severe credit damage |

| Overleveraging | Payment strain |

| Ignoring rate changes | Budget instability |

| Converting unsecured to secured debt carelessly | Increased asset exposure |

Summary

Common mistakes when choosing between secured vs unsecured loans include ignoring asset risk, focusing only on rates, overborrowing, and underestimating default consequences. In a high-interest economy, these errors increase financial instability.

Key Takeaways

- Lower interest does not always mean safer.

- Asset protection should be prioritized.

- Default consequences differ but are serious in both types.

- Rate volatility must be considered.

- Strategic decision-making reduces long-term risk.

Conclusion

Understanding secured vs unsecured loans is essential when borrowing costs are elevated. Both loan types serve different financial needs, but they distribute risk in fundamentally different ways.

Secured loans reduce lender risk through collateral, which typically results in lower interest rates and higher borrowing limits. However, this structure exposes borrowers to asset seizure if repayment fails. In contrast, unsecured loans protect physical property but compensate lenders with higher interest rates and stricter credit standards.

In a high-interest economy, repayment pressure increases for both loan types. Rising benchmark rates influence lending costs across financial markets, often widening the pricing gap between secured and unsecured borrowing. This makes income stability, emergency savings, and risk tolerance more important than ever.

There is no universally safer option. The right choice depends on:

- Stability of income

- Importance of the pledged asset

- Ability to absorb higher interest costs

- Long-term financial resilience

Borrowers who prioritize asset protection may prefer unsecured options despite higher rates. Borrowers with stable income and strong repayment capacity may benefit from secured structures to reduce total borrowing cost.

Ultimately, evaluating secured vs unsecured loans requires balancing cost efficiency with asset security in the context of economic conditions.

Frequently Asked Questions (FAQs)

1. What is the difference between secured and unsecured loan products?

The main difference in secured vs unsecured loans is collateral. Secured loans require an asset pledge, allowing lenders to recover losses through seizure. Unsecured loans do not require collateral and rely on creditworthiness, which typically results in higher interest rates.

2. Which loan type is better in high interest rates?

There is no universal answer. In secured vs unsecured loans, secured options may offer lower interest rates, while unsecured loans protect assets. The better choice depends on income stability, asset importance, and risk tolerance.

3. What happens if you default on a secured loan?

In secured vs unsecured loans, secured default can lead to repossession or foreclosure of the pledged asset. The lender may sell the asset to recover the balance, and the borrower could still owe any remaining deficiency amount.

4. Are unsecured personal loan interest rates always higher?

In most cases, yes. Unsecured personal loan interest rates are generally higher because lenders cannot recover losses through collateral. In high-interest economies, this pricing gap often becomes wider.

5. Can you lose your house with a secured loan?

Yes. If a home is used as collateral in secured vs unsecured loans, default may result in foreclosure. This is one of the primary risks associated with secured borrowing.

6. Does unsecured loan default affect credit score?

Yes. In secured vs unsecured loans, default on either type significantly damages credit scores. Late payments, charge-offs, and collection actions can remain on credit reports for several years.

7. Is a secured loan safer for lenders or borrowers?

Secured loans are generally safer for lenders because collateral reduces recovery risk. For borrowers, safety depends on financial stability and asset importance.

Disclaimer

All information is provided for awareness and general understanding only. It is not financial advice. Always consult a qualified professional before making loan-related decisions.