Managing money during inflation begins with understanding how rising prices reshape personal financial stability. Inflation does not only increase costs temporarily; it steadily reduces purchasing power, alters investment performance, and changes how savings grow over time.

When inflation persists alongside economic uncertainty, households face simultaneous pressure from higher living expenses and unpredictable financial markets. Under these conditions, managing money during inflation becomes a structured financial necessity rather than an optional strategy.

Economic history shows that individuals who adapt early through budgeting adjustments, savings protection, and diversified investments preserve wealth more effectively during inflationary cycles.

What “Managing Money During Inflation” Means for Personal Finance

Managing money during inflation requires aligning income, spending, savings, and investments with changing price levels. Inflation reduces the value of currency, meaning the same salary supports fewer expenses each year.

Key areas directly affected include:

- Food and household essentials

- Housing and rent payments

- Transportation and fuel costs

- Healthcare expenses

- Education and long-term planning

When income growth fails to match inflation, real financial progress slows. As a result, managing money during inflation involves actively adjusting financial behavior instead of relying on traditional saving habits.

Financial planning standards emphasize maintaining purchasing power rather than focusing solely on account balances.

How Rising Prices Affect Managing Money During Inflation

Rising prices gradually weaken purchasing power. Even moderate inflation compounds significantly over time.

For example, consistent inflation between 5–7% can substantially increase living expenses within a decade. Without investment growth exceeding inflation, savings effectively shrink in real terms.

Inflation Impact on Household Expenses

| Expense Category | Normal Economic Period | Inflationary Period |

|---|---|---|

| Groceries | Stable pricing | Frequent increases |

| Housing | Predictable growth | Rapid rent adjustments |

| Utilities | Moderate change | Energy volatility |

| Transportation | Controlled costs | Fuel price swings |

| Healthcare | Gradual rise | Accelerated expenses |

Managing money during inflation therefore requires continuous monitoring of expense categories most sensitive to price increases.

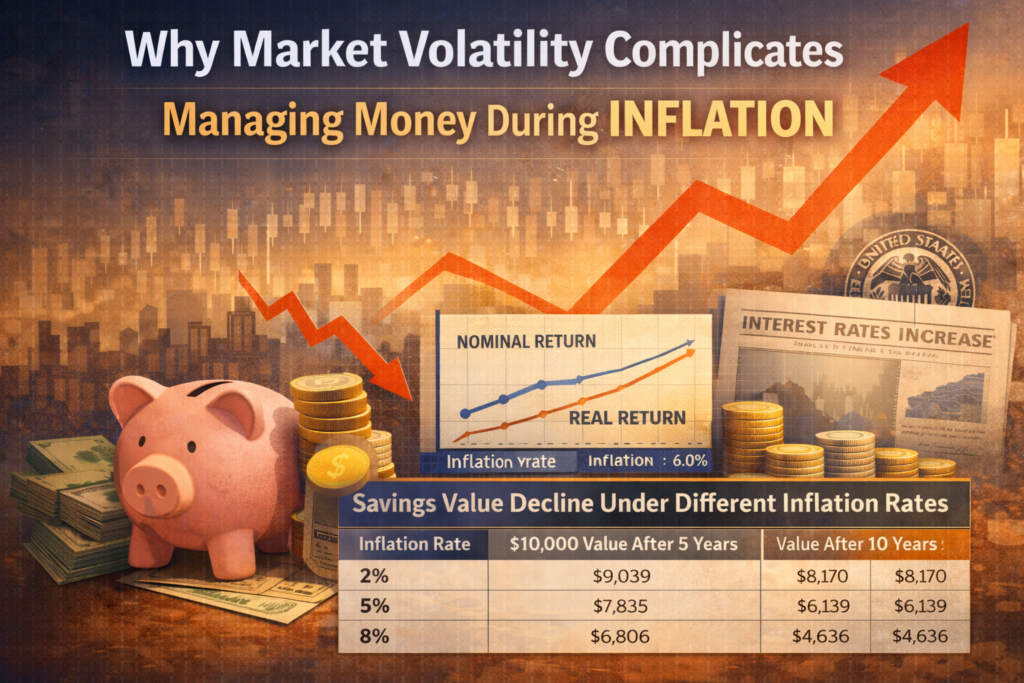

Why Market Volatility Complicates Managing Money During Inflation

Inflation rarely occurs without financial market reactions. Central banks often increase interest rates to control price growth, which affects borrowing, investment returns, and employment conditions.

These adjustments introduce volatility across:

- Stock markets

- Bond markets

- Property valuations

- Business investment activity

Market fluctuations can create uncertainty for investors. However, long-term data indicates that disciplined strategies outperform emotional decision-making.

Managing money during inflation successfully depends on maintaining financial consistency despite short-term market instability.

Real vs Nominal Returns When Managing Money During Inflation

Understanding investment performance is critical.

Nominal Return: Reported investment gain.

Real Return: Gain after accounting for inflation.

If an investment grows by 8% while inflation equals 6%, the real increase in purchasing power is only 2%.

Managing money during inflation requires prioritizing investments capable of delivering positive real returns over extended periods.

How Inflation Affects Savings, Income, and Wealth

Inflation influences wealth accumulation through gradual erosion rather than sudden financial loss. Many individuals underestimate how quickly savings decline when returns lag behind inflation.

Why Cash Savings Challenge Managing Money During Inflation

Cash provides security and liquidity but performs poorly during sustained inflationary environments.

Money held in low-interest accounts steadily loses purchasing power when inflation exceeds earned interest. This silent erosion represents one of the most common financial risks households face.

Savings Value Decline Under Different Inflation Rates

| Inflation Rate | $10,000 Value After 5 Years | Value After 10 Years |

|---|---|---|

| 2% | $9,039 | $8,170 |

| 5% | $7,835 | $6,139 |

| 8% | $6,806 | $4,636 |

Managing money during inflation involves balancing liquidity needs while preventing excessive idle cash exposure.

Real Interest Rates and Managing Money During Inflation

Real interest rates determine whether savings genuinely grow.

Real Interest Rate = Interest Earned − Inflation Rate

When inflation surpasses savings returns, wealth declines despite numerical balance growth. Financial institutions increasingly stress inflation-adjusted planning models to protect long-term capital.

Managing money during inflation requires seeking returns that at minimum match rising price levels.

Retirement Planning Challenges When Managing Money During Inflation

Inflation represents a major long-term retirement risk. Small forecasting errors compound over decades, significantly affecting retirement purchasing power.

Common inflation-related retirement risks include:

- Underestimated living expenses

- Reduced fixed-income value

- Healthcare cost escalation

- Extended longevity expenses

Periodic reassessment of retirement plans ensures financial targets remain realistic under changing economic conditions.

Managing money during inflation therefore includes updating long-term financial projections regularly.

Managing Money During Inflation Through Smart Budgeting During a Cost of Living Crisis

Budgeting becomes the most immediate financial defense during inflationary periods. Static budgets quickly become outdated as prices fluctuate.

Effective households adopt adaptive financial systems.

Inflation-Adjusted Budgeting for Managing Money During Inflation

An inflation-adjusted budget emphasizes flexibility and spending awareness.

Recommended practices include:

- Monthly expense reviews

- Tracking food, housing, and energy costs

- Increasing savings when income rises

- Eliminating unnecessary recurring expenses

Managing money during inflation depends heavily on rapid financial adjustments rather than annual budgeting reviews.

Traditional Budget vs Inflation Budget

| Budget Element | Traditional Budget | Inflation Budget |

|---|---|---|

| Expense Tracking | Annual | Monthly |

| Savings Rate | Fixed | Adjustable |

| Discretionary Spending | Stable | Controlled |

| Emergency Fund | Minimum | Expanded |

| Financial Review | Occasional | Continuous |

Essential vs Discretionary Spending in Managing Money During Inflation

Separating spending categories improves financial control.

Essential Expenses

- Housing

- Utilities

- Food

- Insurance

- Transportation

Discretionary Expenses

- Entertainment

- Luxury purchases

- Non-essential subscriptions

- Lifestyle upgrades

Managing money during inflation requires protecting essential spending while temporarily limiting discretionary consumption.

Practical Recession Budgeting Tips for Managing Money During Inflation

Proven budgeting strategies include:

- Buying durable goods instead of disposable alternatives

- Planning purchases strategically

- Reducing high-interest liabilities

- Avoiding lifestyle expansion during income growth

- Maintaining automated savings contributions

Inflation Survival Rules

- Review expenses monthly

- Maintain emergency liquidity

- Avoid unnecessary debt

- Preserve investment discipline

- Focus on purchasing power growth

Key Takeaway

Managing money during inflation starts with understanding how inflation reshapes savings, spending, and investment outcomes. Individuals who monitor purchasing power, adapt budgets quickly, and prioritize real financial growth build stronger resilience during volatile economic periods.

How Managing Money During Inflation Protects Savings, Income, and Long-Term Wealth

Managing money during inflation becomes significantly more challenging once rising prices begin affecting savings growth, income stability, and long-term financial planning. Inflation does not only increase everyday expenses — it gradually weakens accumulated wealth if financial strategies remain unchanged.

Periods of persistent inflation reshape how money behaves across banking systems, investment markets, and retirement portfolios. Individuals who understand these structural effects can adjust early and prevent long-term financial erosion.

Why Managing Money During Inflation Requires Rethinking Cash Savings

One of the biggest misconceptions in personal finance is believing cash savings automatically provide financial security. While liquidity remains essential, managing money during inflation requires recognizing that idle cash steadily loses purchasing power.

When inflation rises faster than interest earned on savings accounts, the real value of stored money declines year after year.

For example:

| Inflation Rate | Savings Interest | Real Return | Result |

|---|---|---|---|

| 3% | 2% | -1% | Purchasing power declines |

| 6% | 3% | -3% | Wealth erosion accelerates |

| 8% | 4% | -4% | Savings lose value rapidly |

Even though account balances appear stable numerically, households can afford fewer goods and services over time.

This phenomenon explains why managing money during inflation shifts focus from capital preservation alone toward purchasing-power preservation.

Financial planners increasingly emphasize balancing liquidity with growth-oriented financial positioning instead of excessive cash accumulation.

Real Interest Rates and Wealth Erosion During Inflation

A central concept in managing money during inflation is understanding the difference between nominal returns and real returns.

Nominal returns represent the percentage gain shown on financial statements. Real returns measure actual wealth growth after inflation adjustments.

Real Return Formula:

Real Return = Nominal Return − Inflation Rate

If investments generate 7% annually while inflation runs at 6%, real wealth growth equals only 1%.

Institutions such as the International Monetary Fund and the World Bank frequently highlight real interest rates as a primary determinant of long-term household wealth stability.

Negative real rates create silent financial pressure by rewarding borrowing while penalizing savers.

As a result, managing money during inflation requires:

- Monitoring real returns instead of headline yields

- Evaluating savings products relative to inflation trends

- Reallocating funds toward assets capable of long-term growth

Ignoring real return dynamics often leads to gradual but substantial wealth loss.

Managing Money During Inflation and Its Impact on Retirement Planning

Inflation risk becomes especially dangerous in retirement planning because compounding works in reverse when purchasing power declines.

A retirement fund designed decades earlier may appear sufficient in nominal terms yet fail to sustain living standards under prolonged inflation.

Consider this simplified projection:

| Annual Inflation | Monthly Expense Today | Expense After 20 Years |

|---|---|---|

| 3% | $1,000 | $1,806 |

| 5% | $1,000 | $2,653 |

| 7% | $1,000 | $3,870 |

Without inflation-adjusted planning, retirees may experience income shortfalls despite disciplined saving.

Managing money during inflation therefore involves integrating inflation assumptions into retirement strategies through:

- Growth-oriented investment exposure

- Periodic portfolio rebalancing

- Inflation-adjusted withdrawal planning

- Diversified income sources

Many modern retirement frameworks recommended by organizations like the Organisation for Economic Co-operation and Development incorporate inflation stress testing to ensure long-term sustainability.

Income Pressure and Lifestyle Adjustments in Inflationary Periods

Another overlooked aspect of managing money during inflation is wage lag. Prices often rise faster than salaries, creating declining real income even when nominal earnings increase.

This mismatch produces what economists describe as a cost-of-living squeeze.

Households typically experience:

- Higher food and energy costs

- Increased housing expenses

- Rising transportation and healthcare spending

- Reduced discretionary income

Managing money during inflation requires proactive income evaluation rather than reactive spending cuts.

Effective responses include:

- Negotiating inflation-adjusted salary revisions

- Upskilling for higher-income opportunities

- Developing secondary income streams

- Shifting consumption toward value-based spending

Financial resilience increasingly depends on adaptability rather than fixed income expectations.

Inflation’s Compounding Effect on Wealth Inequality

Inflation impacts households differently depending on asset ownership.

Individuals holding appreciating assets often maintain or grow wealth, while those relying solely on wages or cash savings face declining purchasing power.

Central banks such as the Federal Reserve System and the European Central Bank monitor inflation partly because prolonged price instability can widen economic inequality.

Managing money during inflation therefore becomes not just a budgeting exercise but a structural financial decision involving:

- Asset participation

- Investment access

- Financial literacy

- Long-term planning discipline

Those who transition from pure saving toward diversified financial participation generally withstand inflationary cycles more effectively.

Long-Term Wealth Preservation Framework

Successful managing money during inflation follows a layered protection model:

| Financial Layer | Objective | Strategy |

|---|---|---|

| Liquidity | Short-term stability | Emergency savings |

| Protection | Preserve purchasing power | Inflation-aware accounts |

| Growth | Beat inflation | Diversified investments |

| Income | Maintain lifestyle | Multiple revenue streams |

This framework prevents overexposure to any single financial risk during volatile economic environments.

Key Insight

Managing money during inflation is ultimately about aligning financial decisions with economic reality rather than relying on traditional saving habits designed for stable-price environments.

Inflation changes how savings grow, how income performs, and how retirement plans succeed. Individuals who adapt early protect both present financial stability and future wealth potential.

Managing Money During Inflation Through Investment Diversification, and Income Growth

Managing money during inflation ultimately moves beyond understanding economic theory. The real challenge begins when households must actively adjust spending habits, investment decisions, and income strategies to maintain financial stability in volatile markets.

Inflation reshapes daily financial behavior. Traditional budgeting models, passive saving habits, and static income planning often fail when prices rise consistently. A structured financial response becomes essential for protecting purchasing power and sustaining long-term wealth growth.

Managing Money During Inflation With an Inflation-Adjusted Budget

One of the most immediate steps in managing money during inflation is redesigning personal budgets to reflect changing price realities rather than historical spending patterns.

Standard budgets assume relatively stable costs. Inflation disrupts this assumption by increasing recurring expenses such as housing, food, utilities, transportation, and healthcare.

An inflation-adjusted budgeting model separates expenses into essential and flexible categories.

| Expense Category | Traditional Budget Share | Inflation Budget Share |

|---|---|---|

| Housing & Utilities | 30% | 35–40% |

| Food | 12% | 15–18% |

| Transportation | 10% | 12–14% |

| Savings & Investments | 20% | 18–22% |

| Discretionary Spending | 28% | 15–20% |

Managing money during inflation requires protecting savings and investment contributions even when expenses rise. Many households mistakenly reduce investing first, which weakens future financial security.

Effective budgeting adjustments include:

- Reviewing expenses monthly instead of annually

- Eliminating low-value recurring subscriptions

- Prioritizing essential consumption

- Redirecting savings toward inflation-resistant assets

This adaptive budgeting approach improves financial resilience during cost-of-living pressure.

Practical Recession Budgeting Tips for Financial Stability

Periods of inflation often coincide with economic uncertainty or slowing growth. Managing money during inflation therefore overlaps with recession-prepared financial behavior.

Financial planners emphasize defensive strategies designed to increase flexibility.

Key recession-ready actions include:

- Maintaining three to six months of emergency savings

- Avoiding lifestyle inflation during income growth

- Delaying nonessential large purchases

- Increasing savings automation

- Monitoring debt obligations carefully

Economic research published by institutions such as the Bank for International Settlements shows households with liquidity buffers recover faster from economic shocks than those operating with minimal reserves.

Managing money during inflation is less about extreme austerity and more about controlled financial prioritization.

Managing Money During Inflation by Protecting Savings Effectively

Savings remain a critical financial foundation, but inflation changes how savings should be structured.

Instead of holding excessive idle cash, households benefit from layered savings strategies combining accessibility and yield optimization.

Savings protection methods include:

| Method | Inflation Protection Level | Liquidity | Risk Level |

|---|---|---|---|

| Standard Savings Account | Low | High | Very Low |

| High-Yield Savings Accounts | Moderate | High | Low |

| Inflation-Linked Securities | High | Medium | Low |

| Short-Term Bond Funds | Moderate | Medium | Moderate |

Central banks adjust interest rates to combat inflation, which often increases returns on higher-yield savings products. Monitoring policy decisions from organizations like the State Bank of Pakistan helps individuals understand changing savings opportunities.

Managing money during inflation involves ensuring savings maintain real value while remaining accessible for emergencies.

Inflation-Resistant Investment Strategies for Long-Term Growth

Investment diversification becomes one of the most powerful tools for managing money during inflation.

Historically, certain asset classes demonstrate stronger performance during inflationary environments because their values adjust alongside rising prices.

Equity Investments

Stocks represent ownership in companies capable of increasing prices alongside inflation. Businesses with strong pricing power often maintain profitability even when costs rise.

Broad market exposure through index investing allows participation in long-term economic growth rather than reliance on individual company performance.

Real Estate Assets

Real estate frequently acts as an inflation hedge because property values and rental income tend to rise with general price levels.

Property ownership or real estate investment funds can support wealth preservation when currency purchasing power declines.

Commodities and Precious Metals

Physical assets such as energy resources and precious metals historically retain value during inflationary cycles due to supply constraints and global demand.

Inflation-Protected Bonds

Government-issued inflation-linked securities adjust principal values according to inflation rates, helping investors preserve purchasing power.

| Asset Class | Inflation Resistance | Volatility | Long-Term Role |

|---|---|---|---|

| Equities | High | Moderate | Growth |

| Real Estate | High | Moderate | Income + Hedge |

| Commodities | Moderate–High | High | Diversification |

| Inflation Bonds | Moderate | Low | Stability |

Managing money during inflation requires balancing growth potential with risk tolerance rather than concentrating wealth in a single asset type.

Why Diversifying Portfolio Strengthens Financial Security

Diversification reduces exposure to market shocks — a critical principle when managing money during inflation and volatile markets simultaneously.

A diversified portfolio spreads investments across:

- Asset classes

- Geographic markets

- Economic sectors

- Currency environments

Global diversification allows investors to benefit from growth cycles occurring in different economies.

Organizations like the Morgan Stanley frequently emphasize diversification as one of the most reliable long-term risk-management strategies.

Diversification Benefits

| Advantage | Financial Impact |

|---|---|

| Risk reduction | Limits large losses |

| Stable returns | Smooth performance cycles |

| Inflation protection | Multiple growth drivers |

| Market adaptability | Resilience during volatility |

Managing money during inflation becomes significantly more sustainable when investment risks are distributed intelligently.

Debt Management Strategies During Inflationary Periods

Inflation affects borrowers and lenders differently. Understanding this relationship is essential when managing money during inflation.

Fixed-interest debt may become easier to repay because repayments remain constant while currency value declines.

| Debt Type | Inflation Impact |

|---|---|

| Fixed-Rate Loans | Borrower advantage |

| Variable-Rate Loans | Higher payment risk |

| Credit Card Debt | Highly vulnerable |

| Mortgage Debt | Often manageable long term |

However, high-interest consumer debt remains dangerous regardless of inflation conditions.

Priority actions include:

- Paying off high-interest liabilities first

- Avoiding adjustable-rate debt exposure

- Refinancing when interest conditions permit

- Maintaining manageable debt-to-income ratios

Responsible debt positioning strengthens financial flexibility during uncertain economic periods.

Managing Money During Inflation by Expanding Income Sources

Income growth represents one of the most underestimated inflation defenses.

When expenses rise persistently, wealth preservation depends not only on reducing costs but also on increasing earning capacity.

Effective income strategies include:

- Developing freelance or digital income streams

- Investing in skill development

- Building dividend or rental income

- Creating scalable online revenue channels

Labor market studies from the World Economic Forum highlight continuous skill adaptation as a major determinant of income resilience in changing economic environments.

Managing money during inflation therefore combines expense control with income expansion.

Common Financial Mistakes to Avoid During Inflation

Many financial setbacks occur due to emotional reactions rather than economic conditions.

Common mistakes include:

- Holding excessive cash for long periods

- Panic selling investments during volatility

- Ignoring diversification principles

- Increasing lifestyle spending after salary growth

- Making short-term decisions based on market fear

Avoiding these behaviors preserves long-term financial momentum.

Quick Financial Response Framework

| Step | Action |

|---|---|

| 1 | Adjust budget for rising costs |

| 2 | Protect savings from erosion |

| 3 | Diversify investments |

| 4 | Optimize debt structure |

| 5 | Expand income sources |

| 6 | Review financial plan regularly |

Managing money during inflation is not a single decision but an ongoing adaptive process that aligns personal finance strategies with evolving economic conditions.

Conclusion

Managing money during inflation requires disciplined financial planning, adaptive decision-making, and long-term thinking rather than reactive short-term actions. Rising prices reduce purchasing power, increase market uncertainty, and place pressure on savings, income, and investment returns.

A sustainable financial strategy during inflation focuses on five core principles:

- Adjust spending using inflation-aware budgeting

- Protect savings through yield optimization and liquidity planning

- Invest in assets capable of maintaining real returns

- Diversify portfolios to reduce volatility risk

- Strengthen income sources to offset rising living costs

Economic cycles consistently demonstrate that individuals who actively manage money during inflation — instead of relying on static financial habits — are better positioned to preserve wealth and capture future growth opportunities.

Inflation is not only a financial challenge but also a planning test. Structured budgeting, diversified investments, controlled debt exposure, and continuous income development collectively create financial resilience during volatile market environments.

Frequently Asked Questions (FAQs)

1. How can individuals manage money during inflation effectively?

Managing money during inflation involves adjusting budgets, limiting unnecessary spending, protecting savings from value erosion, investing in inflation-resistant assets, and diversifying income streams. Maintaining disciplined financial planning helps preserve purchasing power despite rising prices.

2. What investments help protect wealth during inflation?

Assets historically associated with inflation protection include:

- Equities with strong pricing power

- Real estate investments

- Commodities and precious metals

- Inflation-linked government securities

- Broad market index funds

Diversification across these asset classes reduces long-term inflation risk.

3. Is saving money still useful during inflation?

Yes, saving remains essential. However, managing money during inflation requires placing savings in instruments that generate competitive returns, such as high-yield savings accounts or short-term income assets, rather than holding excessive idle cash.

4. Should I prioritize investing or saving during high inflation?

Both are necessary. Emergency savings provide financial security, while investments help maintain purchasing power over time. A balanced approach — liquidity for short-term needs and investments for long-term growth — is considered financially optimal.

5. How does inflation affect household budgeting?

Inflation increases recurring expenses such as food, housing, and transportation. Households must update budgets frequently, prioritize essential spending, and reduce discretionary costs to maintain savings and investment contributions.

6. Can debt be beneficial during inflation?

Fixed-interest debt may become easier to repay because inflation reduces the real value of future payments. However, high-interest or variable-rate debt can become financially risky if borrowing costs increase.

7. What financial mistakes should be avoided during inflation?

Common mistakes include:

- Holding excessive cash

- Panic selling investments

- Ignoring diversification

- Increasing lifestyle spending unnecessarily

- Making short-term decisions based on market volatility

Avoiding these behaviors improves long-term financial stability.

References

- International Monetary Fund — Inflation and household financial stability research

- World Bank — Global inflation and cost-of-living data

- Bank for International Settlements — Monetary policy and inflation studies

- Federal Reserve — Inflation expectations and interest rate analysis

- Organisation for Economic Co-operation and Development — Household savings and economic resilience reports

Disclaimer

This article is for informational and educational purposes only and does not constitute financial or investment advice. The author is not a licensed financial advisor. Readers should conduct their own research and consult a qualified professional before making financial decisions.