A credit score is a numerical measure of your creditworthiness, used by lenders to determine the likelihood you will repay borrowed money on time. Understanding how to improve credit score begins with knowing what it represents. This number summarizes your financial history, including your repayment patterns, outstanding debt, and credit inquiries. A high credit score opens the door to better loan terms, lower interest rates, and increased financial opportunities, while a low score can limit your options. Building a strong credit score is essential for financial stability and unlocking better loan terms. It also complements long-term financial strategies, such as achieving financial independence and early retirement or managing money effectively during periods of high inflation.

Why Lenders Use Credit Scores

Lenders rely on credit scores as a risk assessment tool. By reviewing your score, they can quickly evaluate whether you are a responsible borrower. This evaluation influences decisions such as loan approval, credit card limits, and interest rates. By understanding how to improve credit score, you can present yourself as a low-risk borrower and gain access to better financial products.

Credit Score Ranges Explained

Credit scores are generally categorized into ranges, each indicating a level of creditworthiness:

| Score Range | Rating | Meaning |

|---|---|---|

| 800–850 | Excellent | Access to the best loan rates and credit offers |

| 740–799 | Very Good | Strong credit, likely qualifies for favorable terms |

| 670–739 | Good | Average credit; may receive standard loan offers |

| 580–669 | Fair | Below-average credit; higher interest rates likely |

| 300–579 | Poor | High-risk borrower; limited access to credit |

Knowing where you fall in these ranges is critical when planning how to improve credit score. Even small improvements can move you into a higher category, which can save significant money over time.

Summary

- A credit score summarizes your creditworthiness in a single number.

- Scores range from 300 to 850; higher scores indicate better credit health.

- Lenders use credit scores to determine loan approvals, limits, and interest rates.

- Understanding your score is the first step in planning how to improve credit score.

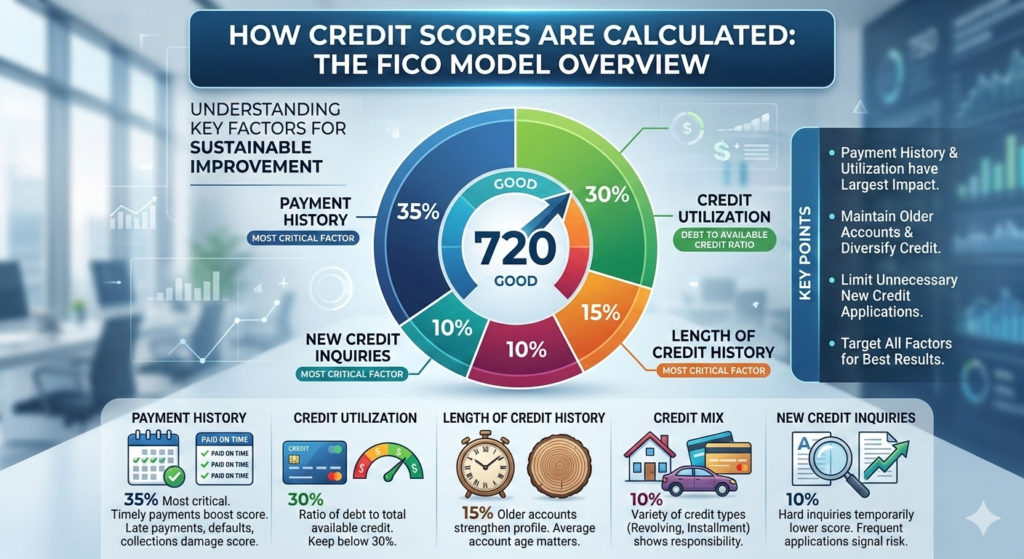

How Credit Scores Are Calculated

Your credit score is determined by several key factors that reflect your financial behavior over time. While different scoring models exist, the FICO Score is the most widely used. Understanding how to improve credit score begins with knowing what affects it. The FICO model evaluates payment history, credit utilization, account age, credit mix, and new credit inquiries to produce a single number representing your creditworthiness. By learning these factors, you can focus on actionable strategies to how to improve credit score effectively.

Overview of the FICO Scoring Model

The FICO scoring model provides a structured way for lenders to assess risk. Scores range from 300 to 850, and each factor contributes differently to the overall score. Knowing these details is essential for anyone serious about how to improve credit score.

| Factor | Weight | Impact |

|---|---|---|

| Payment history | 35% | On-time payments significantly boost score |

| Credit utilization | 30% | Lower utilization shows responsible credit use |

| Length of credit history | 15% | Older accounts strengthen your score |

| Credit mix | 10% | Variety of credit types improves your profile |

| New credit inquiries | 10% | Frequent inquiries can temporarily lower score |

By focusing on these areas, you can apply strategies designed specifically to how to improve credit score efficiently.

Payment History

Payment history is the most important factor in your credit score. Timely payments demonstrate reliability, while late payments, collections, or defaults can severely reduce your score. To truly understand how to improve credit score, make sure to pay all bills on time. Automatic payments or reminders are practical tools to maintain a perfect record and consistently improve your credit standing.

Credit Utilization Ratio

Your credit utilization ratio measures how much credit you are using compared to your total available credit. Maintaining a ratio below 30% is recommended, but aiming lower is even more effective for those seeking to how to improve credit score. High utilization can signal financial strain to lenders and lower your score.

Example Table:

| Credit Limit | Current Balance | Utilization |

|---|---|---|

| $5,000 | $1,000 | 20% |

| $10,000 | $6,000 | 60% |

Keeping utilization low across accounts is one of the fastest and most reliable ways to how to improve credit score.

Length of Credit History

The age of your credit accounts reflects experience in managing credit. Older accounts provide a longer track record, which generally improves your score. Closing long-standing accounts can reduce average account age and potentially lower your score. Maintaining older accounts is an important tactic for anyone aiming to how to improve credit score over the long term.

Credit Mix

A healthy credit mix shows your ability to manage different types of credit responsibly. Revolving credit (like credit cards) combined with installment loans (like auto or mortgage loans) strengthens your profile. While you don’t need every type, a balanced mix is an effective strategy for those looking to how to improve credit score sustainably.

New Credit Inquiries

Applying for new credit generates hard inquiries, which may temporarily reduce your score. Multiple inquiries in a short period can indicate financial stress. Soft inquiries, such as checking your own credit score, do not affect it. Limiting unnecessary credit applications is a critical tactic to how to improve credit score efficiently.

Summary

- Five main factors determine your credit score: payment history, credit utilization, account age, credit mix, and new inquiries.

- Payment history and utilization have the largest influence.

- Focusing on all factors consistently is essential to how to improve credit score.

Takeaways

- Always pay bills on time to maintain a strong credit profile.

- Keep credit utilization below 30% to maximize impact on your score.

- Preserve older accounts and maintain a balanced credit mix.

- Limit unnecessary new credit applications to avoid temporary drops.

- Following these strategies ensures you consistently how to improve credit score over time.

How to Check Your Credit Report

Understanding how to improve credit score requires knowing what your credit report contains. Your credit report is a detailed record of your borrowing and repayment history, maintained by credit reporting agencies. Reviewing your credit report regularly helps you identify errors, spot potential fraud, and understand which factors are impacting your score the most.

Why Reviewing Credit Reports Is Important

Checking your credit report is a crucial step in how to improve credit score. Even small mistakes, such as incorrect account balances or outdated information, can negatively affect your credit. By reviewing your report, you can:

- Verify the accuracy of reported accounts and balances

- Identify late payments or collections that may need correction

- Detect signs of identity theft or fraudulent activity

- Make informed decisions about managing your credit

Where to Check Your Credit Report

In the United States, you are entitled to one free credit report per year from each of the three major credit bureaus. Accessing your report is simple and provides valuable insights for improving your credit score:

Experian

Experian allows you to view your credit history, including accounts, payment history, and credit inquiries. Regularly checking your report helps you track progress and verify accuracy.

Equifax

Equifax provides a full overview of your credit report and alerts for suspicious activity. Correcting errors found on Equifax can have a positive impact on your score.

TransUnion

TransUnion offers detailed reports and monitoring tools to help consumers understand their credit profile. Monitoring this report is essential for anyone serious about how to improve credit score.

How to Identify Errors in Credit Reports

Mistakes on your credit report are more common than many people realize. Common errors include:

- Accounts that don’t belong to you

- Incorrect balances or payment histories

- Outdated personal information

- Duplicate listings of the same debt

Disputing errors promptly with the credit bureau can remove negative items and improve your score. Correcting even minor inaccuracies is a key strategy when learning how to improve credit score.

Summary

- Your credit report contains a detailed record of all your credit activity.

- Checking reports regularly helps identify errors and fraudulent accounts.

- Correcting inaccuracies can improve your credit score and financial credibility.

Takeaways

- Request your free credit report from Experian, Equifax, and TransUnion at least once a year.

- Carefully review all accounts, balances, and personal information for errors.

- Dispute inaccuracies promptly to ensure your score reflects your true creditworthiness.

10 Proven Ways to Improve Your Credit Score

Improving your credit score doesn’t happen overnight, but following proven strategies can accelerate your progress. Understanding how to improve credit score and applying these methods consistently will help you achieve a stronger financial profile and access better loan terms.

1. Pay Bills on Time Consistently

Your payment history is the most significant factor affecting your credit score. Late payments, defaults, or collections can severely damage your score. To improve your credit score, pay all bills on or before the due date. Setting up automatic payments or calendar reminders ensures you never miss a payment.

2. Reduce Credit Utilization Ratio

Maintaining a low credit utilization ratio is one of the fastest ways to increase credit score fast. Aim to use less than 30% of your available credit across all accounts. Paying down balances regularly and spreading charges across multiple cards can keep your utilization low.

3. Avoid Unnecessary Credit Inquiries

Each application for new credit generates a hard inquiry, which can temporarily lower your score. Only apply for credit when necessary, and avoid multiple applications in a short period. Soft inquiries, such as checking your own score, do not affect your rating.

4. Maintain Older Credit Accounts

The age of your credit accounts contributes to your overall score. Closing old accounts can shorten your credit history and reduce your score. Keeping older accounts open, even if they are not used frequently, is an effective long-term strategy to improve credit score.

5. Diversify Credit Mix Responsibly

A varied credit mix—including revolving credit (credit cards) and installment loans (personal or auto loans)—demonstrates responsible credit management. While you don’t need every type of credit, maintaining a balanced mix can positively influence your score.

6. Dispute Inaccurate Credit Report Items

Errors on your credit report, such as incorrect balances or accounts that aren’t yours, can hurt your score. Regularly review your reports from Experian, Equifax, and TransUnion and dispute inaccuracies promptly. Correcting errors is a critical step in how to improve credit score.

7. Set Up Automatic Payments

Automatic payments ensure you never miss a due date. Even one missed payment can significantly reduce your score. Using automatic payments for loans and credit cards is a simple, effective method to increase credit score fast.

8. Request Credit Limit Increases

Raising your credit limits without increasing balances reduces your credit utilization ratio, which can positively impact your score. This strategy works best when your payment habits are already strong.

9. Become an Authorized User

Being added as an authorized user on a responsible person’s credit card can improve your credit score. This allows you to benefit from their positive payment history and low utilization, making it a valuable tool in your plan to improve credit score.

10. Use Credit Monitoring Tools

Credit monitoring services provide real-time updates on changes to your credit report. They alert you to errors, suspicious activity, or sudden drops in score. Using these tools allows you to proactively manage your credit and implement strategies to increase credit score fast.

Summary

Key Points:

- Timely payments and low credit utilization are the most impactful factors.

- Maintaining older accounts and a balanced credit mix supports long-term score growth.

- Disputing errors and monitoring your credit ensures your score reflects your true financial behavior.

Takeaways

- Consistent, responsible credit management is essential to improve credit score.

- Combining short-term strategies (like reducing utilization) with long-term habits (like account age and mix) yields the best results.

- Regularly review your reports and monitor your credit to stay on track.

How to Improve Credit Score Fast

For many, waiting months or years to improve credit can be frustrating. Understanding how to improve credit score quickly requires focusing on strategies that have the most immediate impact. While long-term habits are essential, certain actions can accelerate your score improvement in weeks rather than months.

Rapid Score Improvement Strategies

- Pay Down High Credit Card Balances

Reducing your credit utilization ratio is one of the fastest ways to increase credit score fast. Focus on paying down cards that are near their limits first, aiming to keep utilization below 30%, and ideally around 10–20%. - Correct Errors on Your Credit Report

Mistakes, such as inaccurate balances, old accounts, or duplicate entries, can drag down your score. Reviewing your credit reports and disputing errors with Experian, Equifax, or TransUnion can lead to immediate score increases once corrected. - Become an Authorized User

Adding yourself to a trusted individual’s credit card account with a long, positive payment history can boost your score quickly. This allows you to leverage their strong credit habits without taking on new debt. - Request a Credit Limit Increase

Increasing your credit limits while keeping balances the same reduces your credit utilization ratio, which can positively impact your score in a short time. - Consolidate or Pay Off Small Debts

Paying off multiple small debts or consolidating them can reduce the number of outstanding accounts and improve your payment history, giving your score a noticeable boost.

Short-Term vs Long-Term Credit Improvements

While rapid strategies can provide quick gains, sustainable improvement requires long-term habits:

| Strategy Type | Examples | Timeline for Results |

|---|---|---|

| Short-Term | Reduce utilization, dispute errors, become authorized user | Weeks to 1 month |

| Long-Term | Consistent on-time payments, maintain old accounts, diversify credit mix | 6–24 months |

Focusing on both short-term and long-term strategies ensures immediate improvements while building lasting credit strength.

Factors That Change Credit Scores Quickly

Certain actions can impact your credit score faster than others:

- Credit utilization adjustments – paying down balances can improve scores in a few reporting cycles.

- Error corrections – removing incorrect negative items can immediately raise your score.

- New account activity – opening or closing accounts may have a temporary effect but can be strategically managed.

By understanding how to improve credit score efficiently, you can prioritize the steps that produce measurable results quickly, while also establishing habits for long-term credit health.

Summary

Key Points:

- Reducing credit utilization and correcting errors are the fastest ways to improve your score.

- Becoming an authorized user or increasing credit limits can provide rapid benefits.

- Combining short-term tactics with long-term credit habits ensures lasting improvement.

Takeaways

- Quick improvements are possible, but sustainable growth requires ongoing responsibility.

- Focus on strategies with the largest immediate impact, like utilization and report corrections.

- Always monitor your credit after taking rapid improvement actions to track progress.

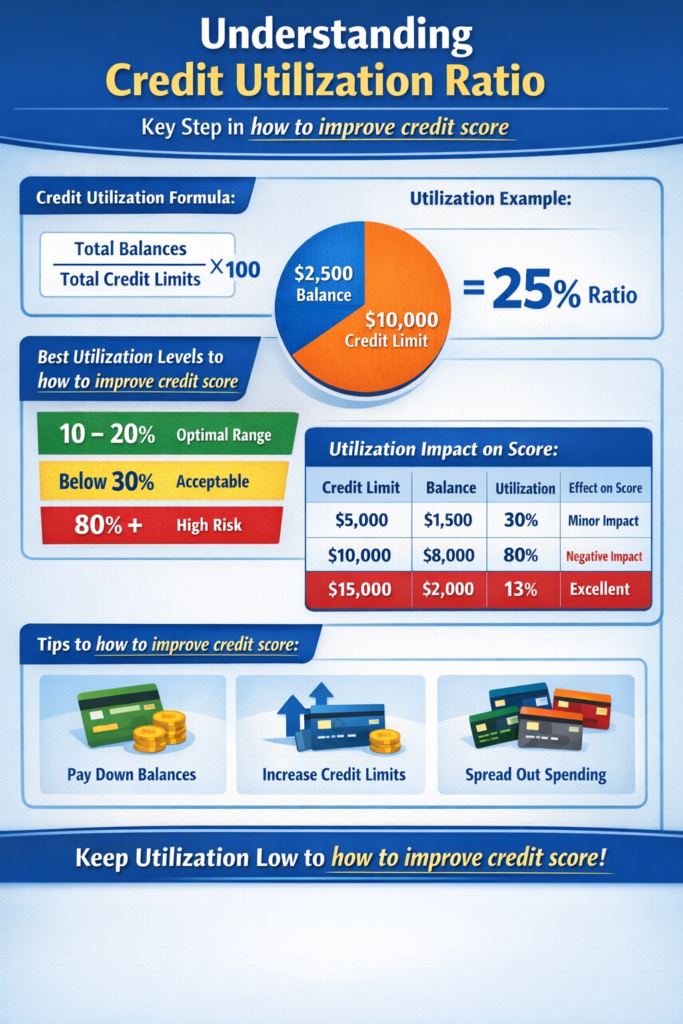

Understanding Credit Utilization Ratio

A critical step in how to improve credit score is understanding your credit utilization ratio. This ratio measures the amount of credit you are using compared to your total available credit and plays a major role in determining your credit score. Maintaining a healthy credit utilization is one of the fastest and most effective strategies to increase credit score fast.

Definition and Formula

The credit utilization ratio is calculated as:Credit Utilization Ratio=Total Credit LimitsTotal Credit Card Balances×100

For example, if your combined credit limit across all cards is $10,000 and your total balance is $2,500, your utilization ratio is 25%. Keeping this ratio low is a proven method to improve credit score efficiently.

Recommended Utilization Percentages

Experts recommend maintaining your utilization below 30%, but the optimal range for those actively trying to improve credit score is between 10% and 20%. High utilization ratios, even temporarily, can signal to lenders that you are over-reliant on credit, which may reduce your score.

Example Table:

| Total Credit Limit | Current Balance | Credit Utilization | Effect on Score |

|---|---|---|---|

| $5,000 | $1,500 | 30% | Acceptable, minor impact |

| $10,000 | $8,000 | 80% | Negative impact |

| $15,000 | $2,000 | 13% | Optimal for improving score |

By consistently keeping your utilization low, you can increase credit score fast and demonstrate responsible credit management.

How Utilization Impacts Credit Scores

The credit utilization ratio is one of the largest factors influencing your credit score after payment history. High utilization can lower your score quickly, while lowering balances can improve your score in just one or two billing cycles. When learning how to improve credit score, focusing on utilization management should be a top priority.

Practical strategies include:

- Paying down balances before the statement date

- Spreading charges across multiple cards to avoid high utilization on a single card

- Requesting a credit limit increase while maintaining low balances

By implementing these strategies, you not only reduce your utilization ratio but also take a significant step toward long-term credit health and achieving your goal of how to improve credit score.

Summary

Key Points:

- Credit utilization ratio measures your used credit versus total available credit.

- Keeping utilization below 30%, ideally 10–20%, is essential to improve credit score.

- Reducing high balances quickly can lead to noticeable improvements.

Takeaways

- Monitoring and managing utilization is a fast, actionable way to increase credit score fast.

- Paying balances early and spreading usage across accounts helps optimize utilization.

- Combining utilization management with on-time payments maximizes score improvements.

Common Credit Score Myths

Many people struggle to improve their credit score because they believe common myths that are not true. Understanding these misconceptions is a critical step in how to improve credit score effectively. Separating fact from fiction allows you to focus on strategies that genuinely impact your credit health.

Myth 1: Checking Your Credit Hurts Your Score

One of the biggest myths is that checking your own credit report or score will lower it. In reality, checking your own score is a soft inquiry and does not affect your credit rating. Learning this is essential for anyone trying to improve credit score, because monitoring your reports helps identify errors and track progress.

Myth 2: Closing Credit Cards Improves Your Score

Some believe that closing old or unused credit cards can help improve their credit score. In fact, closing accounts can lower your average account age and increase your credit utilization ratio, which can reduce your score. To truly improve credit score, it’s often better to keep older accounts open, even if you use them sparingly.

Myth 3: Carrying a Balance Improves Your Score

Many think that carrying a balance on credit cards helps improve credit. This is false. Maintaining a low utilization ratio is more important. Carrying debt unnecessarily can harm your score. Understanding this is crucial in any plan for how to improve credit score.

Myth 4: Income Affects Credit Score

While income influences your ability to repay loans, it does not directly impact your credit score. Credit scoring models focus on your repayment history, credit utilization, and account management. Knowing this helps you focus on the real strategies to increase credit score fast.

Myth 5: Paying Off Collections Immediately Always Helps

Although paying off collections is important for financial health, it does not always immediately raise your score. However, resolving collections prevents further negative reporting and positions you to improve credit score over time.

Summary

Key Points:

- Many common beliefs about credit are myths that can mislead you when learning how to improve credit score.

- Checking your own credit, closing old accounts, or carrying a balance are often misunderstood practices.

- Focusing on payment history, credit utilization, and account management is the true path to improving your score.

Takeaways

- Avoid following myths that do not impact your score; focus on actionable strategies for how to improve credit score.

- Regularly review your credit reports to identify errors.

- Keep older accounts, manage balances, and monitor utilization to increase credit score fast.

Long-Term Strategies for Maintaining a High Credit Score

Once you understand how to improve credit score, it’s essential to implement long-term strategies to maintain and grow your creditworthiness. Quick fixes can help temporarily, but lasting financial health requires consistent habits that target the key factors impacting your score. Following these strategies ensures that your efforts to improve credit score are sustainable and effective over time.

Responsible Credit Habits

Maintaining a strong credit profile begins with responsible credit habits, which are the foundation of how to improve credit score. This includes:

- Paying bills on time: Late payments can significantly lower your score, so consistent timely payments are essential to maintaining high credit health.

- Managing credit utilization ratio: Keep balances low relative to your credit limits, ideally below 30%. This is one of the fastest and most reliable ways to increase credit score fast.

- Avoiding unnecessary debt: Only take on credit you can repay responsibly to prevent negative impacts on your score.

By embedding these habits into your financial routine, you create a foundation for long-term improvement and a stronger ability to improve credit score continuously. Maintaining a high credit score over time is not just about timely payments and low utilization—it supports your broader financial goals, including preparing for early retirement through FIRE principles and managing money during inflation to protect your wealth effectively

Monitoring Credit Regularly

Monitoring your credit reports and scores is a critical part of how to improve credit score over time. Regular reviews help you:

- Identify errors that may drag down your score

- Detect fraudulent activity early

- Track your progress on strategies designed to increase credit score fast

Using credit monitoring tools or checking reports from Experian, Equifax, and TransUnion ensures you stay informed and proactive in maintaining your credit health.

Financial Planning and Debt Management

Long-term credit success relies on proper financial planning and debt management, which directly impacts your ability to improve credit score. Consider these approaches:

- Budgeting effectively: Plan monthly expenses to avoid overspending and ensure timely payments.

- Strategic debt repayment: Prioritize high-interest or high-utilization accounts to reduce your overall credit utilization ratio, which can increase credit score fast.

- Maintaining a balanced credit mix: Use both revolving and installment credit responsibly to strengthen your profile over time.

These practices support sustainable improvement and reinforce the habits necessary to continually improve credit score.

Summary

Key Points:

- Long-term credit improvement focuses on consistent, responsible habits.

- Regular monitoring, budgeting, and strategic debt management are essential to how to improve credit score.

- Keeping utilization low, paying on time, and maintaining a healthy credit mix ensures sustained growth.

Takeaways

- Establish daily financial habits that promote strong credit.

- Monitor credit reports and scores to identify opportunities to increase credit score fast.

- Combine responsible usage, debt management, and account diversity to maximize long-term score improvement.

- Consistency is the key to maintaining and improving your credit health over time.

Conclusion

Improving your credit profile is not just about short-term tactics—it’s about building lasting financial habits. Understanding how to improve credit score is essential for accessing better loan terms, lower interest rates, and broader financial opportunities. By consistently paying bills on time, maintaining a low credit utilization ratio, keeping older accounts open, diversifying your credit mix, and monitoring your credit reports, you can steadily how to improve credit score over time.

Remember, both short-term actions—like paying down high balances or correcting errors—and long-term strategies—like responsible credit management and strategic account maintenance—work together to strengthen your creditworthiness. Applying these proven methods will ensure you not only how to improve credit score quickly but also sustain a healthy financial profile for years to come.

Key Takeaways:

- Consistent on-time payments and low utilization are the foundation of credit health.

- Monitoring your credit reports helps identify areas to how to improve credit score efficiently.

- Combining short-term strategies with long-term habits ensures sustainable improvement.

- Understanding the factors that affect your credit score is the first step to how to improve credit score successfully.

FAQs

1. What is the fastest way to improve credit score?

The fastest way to improve credit score is to lower your credit utilization, correct errors on your credit reports, and ensure timely payments. Strategic short-term actions like becoming an authorized user or requesting a credit limit increase can also boost your score quickly. These steps directly support your plan for how to improve credit score efficiently.

2. How long does it take to improve credit score?

Improving your credit score depends on the actions you take. Paying bills on time and maintaining low balances can show results in weeks, while establishing a long-term payment history and diversifying credit may take several months. Combining short-term and long-term strategies is key to how to improve credit score effectively.

3. How can I check my credit report without affecting my score?

You can check your credit report through Experian, Equifax, or TransUnion for free once a year. These soft inquiries do not lower your score but help identify errors or areas to focus on to how to improve credit score.

4. What is a good credit utilization ratio to improve my credit score?

Experts recommend keeping your credit utilization below 30%, with an optimal range of 10–20% for faster improvement. Managing utilization consistently is one of the most important steps in how to improve credit score.

5. Do credit card inquiries lower my credit score?

Yes, hard inquiries from applying for new credit can temporarily lower your score. Limiting unnecessary applications and planning inquiries carefully are essential strategies for how to improve credit score without unwanted drops.

6. Can becoming an authorized user improve my credit score?

Yes, being added as an authorized user on a responsible person’s credit card can positively impact your score. This approach is an effective method for how to improve credit score quickly while leveraging another person’s strong credit habits.

7. Are there myths that can prevent me from improving my credit score?

Absolutely. Common myths—like carrying a balance improves your score or income affects your score—can mislead you. Focusing on actionable steps is critical for how to improve credit score accurately and efficiently.

Disclaimer:

The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. The author is not a licensed financial advisor. Readers should conduct their own research and consult a qualified financial professional before making any financial or investment decisions.