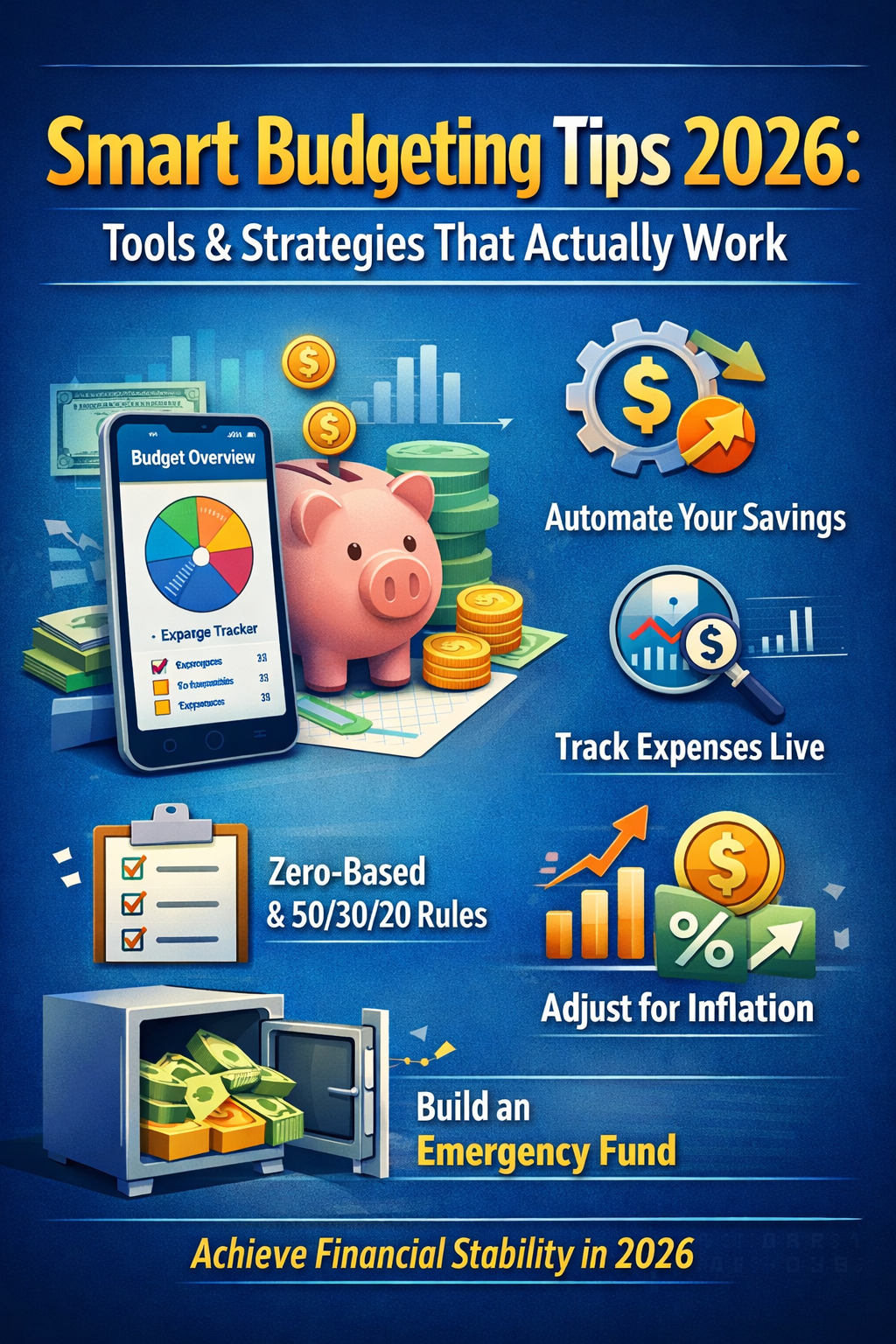

Budgeting tips 2026 reflect a financial system that is automated, data-driven, and inflation-aware. Unlike traditional budgeting methods that relied on manual spreadsheets and fixed monthly allocations, modern budgeting integrates AI-powered tools, real-time expense tracking, and automated savings systems to improve financial control and long-term stability.

In 2026, effective budgeting is no longer about tracking expenses after they happen. It is about building systems that automatically allocate income, categorize transactions, and adjust spending based on economic conditions. This structural shift is what defines budgeting tips 2026.

Modern budgeting emphasizes:

- Automation over manual transfers

- Real-time financial visibility

- Subscription monitoring

- Inflation-adjusted allocation strategies

These elements make budgeting proactive rather than reactive.

Economic Volatility and Inflation Adjustment

Global economic fluctuations have reshaped household financial planning. Institutions such as the Federal Reserve and the OECD report that interest rate variability and inflation directly affect borrowing costs and purchasing power.

As a result, budgeting tips 2026 recommend:

- Reviewing budgets quarterly instead of annually

- Prioritizing high-interest debt repayment

- Increasing emergency savings buffers

- Adjusting expense categories based on inflation trends

Static budgeting models that ignore economic shifts are less effective in the current environment.

The Subscription Economy and Digital Spending

Digital services now represent a consistent portion of monthly expenses. Streaming platforms, SaaS subscriptions, online memberships, and app-based services create recurring micro-payments that accumulate over time.

Budgeting tips 2026 emphasize structured subscription management, including:

- Separating recurring expenses into a dedicated category

- Conducting quarterly subscription audits

- Using digital budgeting tools for automatic alerts

- Eliminating underused services

Visibility into recurring payments is now essential for accurate financial planning.

AI and Automation in Financial Planning

Artificial intelligence plays a central role in modern budgeting systems. Many personal finance platforms use machine learning to automatically categorize expenses, detect unusual spending patterns, and forecast short-term cash flow gaps.

This automation enables:

- Scheduled transfers to savings accounts

- Predictive alerts for overspending

- Automated expense categorization

- Data-driven savings recommendations

Budgeting tips 2026 prioritize automation-first systems because they reduce manual errors and improve financial consistency.

Embedded Definition for Search & AI Extraction

Budgeting tips 2026 focus on automation, AI-driven expense tracking, subscription visibility, and inflation-adjusted financial planning. Modern budgeting systems use digital tools to allocate income automatically, monitor recurring charges, and forecast cash flow, improving financial stability and long-term resilience.

Summary

Budgeting looks different in 2026 because economic volatility, digital spending patterns, and AI-powered tools have transformed personal finance management. The most effective budgeting tips 2026 integrate automation, real-time monitoring, and adaptive financial planning to maintain purchasing power and improve financial control.

What Are the Most Effective Budgeting Tips 2026?

The most effective budgeting tips 2026 focus on automation, structured allocation, real-time tracking, and inflation-aware financial planning. In a digital economy where transactions happen instantly and recurring payments accumulate quietly, budgeting must be proactive rather than reactive.

Modern budgeting is no longer just about cutting expenses. It is about building a financial system that allocates income efficiently, protects purchasing power, and improves long-term stability.

Automate Savings First

One of the most practical budgeting tips 2026 is to automate savings immediately after income is received. Saving what is left at the end of the month often leads to inconsistency. Automated transfers ensure savings happen before discretionary spending begins.

Common automation methods include:

- Direct payroll allocation to savings

- Scheduled bank transfers

- Round-up savings programs

- Percentage-based auto-deposit rules

When savings are automated, consistency improves and financial discipline becomes system-driven rather than emotion-driven.

Track Expenses in Real Time

Digital payments and subscription services require continuous monitoring. Real-time expense tracking allows individuals to see spending patterns instantly rather than reviewing them weeks later.

Effective budgeting tips 2026 recommend:

- Weekly spending reviews

- Automatic transaction categorization

- Alerts for unusual spending

- Separate tracking for recurring subscriptions

Small recurring charges can significantly reduce savings capacity if left unnoticed.

Apply a Structured Budgeting Framework

Structured frameworks provide clarity and control. Two widely used approaches remain effective:

Zero-based budgeting assigns every dollar of income a specific purpose before spending begins. Income minus expenses equals zero because all funds are allocated intentionally.

The 50/30/20 rule divides after-tax income into three categories:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

Budgeting tips 2026 suggest choosing a framework based on income stability and personal preference. Zero-based budgeting offers precision, while the 50/30/20 rule offers simplicity and flexibility.

Adjust for Inflation and Interest Rates

Inflation reduces purchasing power, and interest rate changes affect borrowing costs. Budgets that remain unchanged for years often lose effectiveness.

Strong budgeting tips 2026 include:

- Reviewing allocations quarterly

- Increasing savings contributions when income grows

- Prioritizing repayment of high-interest debt

- Adjusting discretionary spending during inflation spikes

Regular adjustments help maintain financial balance despite economic fluctuations.

Build a 3–6 Month Emergency Fund

An emergency fund protects against unexpected job loss, medical expenses, or urgent repairs. A practical target is three to six months of essential expenses.

| Monthly Expenses | 3-Month Fund | 6-Month Fund |

|---|---|---|

| $2,000 | $6,000 | $12,000 |

| $3,000 | $9,000 | $18,000 |

| $5,000 | $15,000 | $30,000 |

Maintaining this buffer reduces reliance on high-interest credit during financial stress.

In summary, the most effective budgeting tips 2026 emphasize automation, real-time monitoring, structured allocation methods, inflation awareness, and emergency preparedness. Together, these elements create a resilient budgeting system designed for modern financial conditions.

Zero-Based Budgeting vs 50/30/20 Rule (2026 Comparison)

Choosing the right framework is one of the most important budgeting tips 2026 for maintaining control over income and expenses. While many digital tools support multiple methods, two approaches remain widely used: zero-based budgeting and the 50/30/20 rule. Each offers different advantages depending on income stability, financial goals, and automation preferences.

Understanding how these systems work helps determine which structure aligns best with modern financial conditions.

What Is Zero-Based Budgeting?

Zero-based budgeting is a method where every dollar of income is assigned a specific purpose before the month begins. Income minus allocated expenses equals zero because all funds are intentionally distributed across categories such as housing, savings, debt repayment, and discretionary spending.

Key characteristics:

- Detailed income allocation

- High spending visibility

- Strong control over discretionary expenses

- Suitable for variable income management

In 2026, zero-based budgeting works particularly well when paired with digital budgeting tools that automatically track and categorize transactions. This reduces the manual effort traditionally associated with the method.

What Is the 50/30/20 Rule?

The 50/30/20 rule divides after-tax income into three simplified categories:

- 50% for needs (housing, utilities, groceries, insurance)

- 30% for wants (entertainment, dining, subscriptions)

- 20% for savings and debt repayment

This method prioritizes simplicity and ease of use. It requires less detailed tracking than zero-based budgeting and works well for individuals with stable income and predictable expenses.

Among practical budgeting tips 2026, this rule remains effective for those who prefer structure without extensive category management.

Comparison

| Feature | Zero-Based Budgeting | 50/30/20 Rule |

|---|---|---|

| Allocation Style | Detailed, category-level | Broad percentage split |

| Time Requirement | Higher | Lower |

| Control Level | Very High | Moderate |

| Flexibility | High | Moderate |

| Best For | Variable income, aggressive goals | Stable income, simplicity |

| Automation Compatibility | Strong with apps | Easy to automate percentages |

Which Works Better in 2026?

The best option depends on financial complexity and personal goals.

Zero-based budgeting offers greater precision and control, making it suitable for debt reduction plans, irregular income streams, or aggressive savings targets. It aligns well with structured budgeting tips 2026 that emphasize detailed financial visibility.

The 50/30/20 rule provides clarity and simplicity. It is effective for individuals seeking balanced allocation without intensive tracking. Automated percentage transfers make it easy to implement.

In practice, many households combine both methods — using the 50/30/20 rule as a high-level guide and applying zero-based budgeting within specific categories.

Summary

Selecting the right framework is not about choosing the “best” method universally. It is about aligning structure with income patterns, financial goals, and the level of control required. Strong budgeting tips 2026 focus on adaptability, precision, and sustainability rather than rigid adherence to a single system.

Best Budgeting Apps & Digital Budgeting Tools in 2026

Digital tools play a central role in implementing effective budgeting tips 2026. Manual spreadsheets are no longer sufficient for managing subscription-based expenses, variable income, and automated savings systems. Modern budgeting apps provide real-time tracking, automatic categorization, and integrated financial dashboards that improve accuracy and efficiency.

The right digital budgeting tools reduce manual errors, increase visibility, and support long-term financial planning.

AI-Powered Personal Finance Apps

Several established platforms dominate the personal finance space in 2026. These tools integrate bank syncing, automated expense categorization, and savings insights.

Some widely used budgeting apps include:

- YNAB

- PocketGuard

- EveryDollar

- Empower

- Rocket Money

These platforms support structured budgeting tips 2026 by offering:

- Automatic transaction imports

- Smart expense categorization

- Custom budget categories

- Net worth tracking

- Financial goal monitoring

Automation ensures budgets update dynamically rather than requiring manual data entry.

Subscription Tracking Tools

Recurring digital payments have become a significant portion of monthly spending. Streaming services, SaaS tools, and online memberships can accumulate quickly.

Apps like Rocket Money specialize in identifying recurring charges and highlighting underused services. Subscription visibility helps prevent small recurring payments from quietly reducing savings potential.

Effective budgeting tips 2026 recommend reviewing recurring payments at least quarterly and canceling non-essential services.

Automated Savings Platforms

Automation strengthens financial discipline. Many banking platforms now allow rule-based transfers, including:

- Percentage-based savings allocations

- Round-up transfers from purchases

- Automatic emergency fund contributions

- Goal-based savings buckets

High-yield savings accounts also improve returns on reserved funds. According to financial regulatory standards set by organizations such as the Consumer Financial Protection Bureau, consumers should compare account fees, interest rates, and withdrawal terms before selecting savings products.

Automation reduces the psychological barrier to saving and aligns directly with practical budgeting tips 2026.

Comparison of Leading Budgeting Apps

| App | Automation Level | Best For | Key Strength |

|---|---|---|---|

| YNAB | High | Zero-based budgeting users | Detailed allocation control |

| PocketGuard | High | Overspending control | “Safe to Spend” feature |

| EveryDollar | Moderate | Simplicity seekers | Easy monthly planning |

| Empower | High | Net worth tracking | Investment integration |

| Rocket Money | High | Subscription monitoring | Recurring expense alerts |

The best choice depends on financial goals, income stability, and desired level of control.

Security and Data Privacy Considerations

Financial data protection is essential when using digital budgeting tools. Reputable apps use encryption standards, secure data aggregation systems, and multi-factor authentication to protect user information.

When selecting tools, individuals should evaluate:

- Bank-level encryption

- Two-factor authentication

- Transparent data-sharing policies

- Regulatory compliance

Secure systems ensure that budgeting tips 2026 are implemented without increasing cybersecurity risks.

Summary

Digital budgeting tools have transformed how households manage money. By combining automation, real-time tracking, and structured frameworks, these platforms make budgeting more precise and sustainable. Integrating the right tools strengthens the practical application of budgeting tips 2026 and supports consistent financial growth.

How to Automate Savings in 2026 (Step-by-Step)

Automation is one of the most practical budgeting tips 2026 for improving consistency and reducing financial stress. Saving manually often leads to irregular contributions, especially when expenses fluctuate. Automated systems remove friction and ensure savings occur before discretionary spending.

In 2026, automation is not optional for efficient budgeting. It is a core component of modern financial management.

Step 1: Set a Fixed Savings Percentage

Start by determining a fixed percentage of after-tax income to allocate toward savings. Many households follow a minimum 20% savings benchmark, though the exact figure depends on income stability and financial goals.

Automation works best when:

- The percentage is realistic and sustainable

- Transfers are scheduled immediately after payday

- Savings categories are clearly defined (emergency fund, investments, short-term goals)

Allocating savings first aligns with the strongest budgeting tips 2026 principles: prioritize future security before lifestyle spending.

Step 2: Use Payroll Auto-Allocation

Many employers allow direct deposit splitting into multiple accounts. This enables income to be automatically divided between checking and savings accounts at the time of payment.

Benefits include:

- No manual transfers required

- Reduced temptation to overspend

- Immediate allocation discipline

Payroll automation creates a structural saving habit without relying on monthly decisions.

Step 3: Enable Rule-Based Bank Transfers

Most digital banking platforms allow scheduled or rule-based transfers. Examples include:

- Weekly fixed transfers

- Percentage-based transfers

- Threshold-based transfers when account balances exceed a set amount

This system ensures that surplus funds move into savings automatically, reinforcing practical budgeting tips 2026.

Step 4: Activate Round-Up Savings

Round-up automation transfers the difference between a purchase amount and the next whole number into savings. For example, a $3.60 purchase rounds up to $4.00, with $0.40 saved.

Over time, these micro-savings accumulate without noticeable impact on daily spending.

Round-up systems are particularly effective for:

- Individuals new to saving

- Building emergency funds gradually

- Strengthening savings habits without large commitments

Step 5: Automate Emergency Fund Growth

Emergency funds should cover three to six months of essential expenses. Automation ensures steady progress toward this goal.

| Monthly Essential Expenses | 3-Month Target | 6-Month Target |

|---|---|---|

| $2,500 | $7,500 | $15,000 |

| $4,000 | $12,000 | $24,000 |

| $6,000 | $18,000 | $36,000 |

Automatic contributions prevent inconsistent funding and reduce reliance on credit during unexpected events.

Step 6: Review and Adjust Quarterly

Automation does not eliminate the need for oversight. Budget reviews should occur at least quarterly to account for:

- Income increases

- Inflation changes

- Debt reduction progress

- New financial goals

Adjusting automated transfers ensures the system remains aligned with evolving financial conditions.

Summary

Automating savings transforms budgeting from a reactive process into a structured financial system. By setting percentage-based transfers, splitting payroll deposits, enabling rule-based banking, and maintaining consistent reviews, individuals strengthen the practical application of budgeting tips 2026 and improve long-term financial stability.

Creating a Monthly Budget Template for 2026

A structured monthly budget template transforms budgeting tips 2026 from theory into daily financial practice. While apps automate tracking, a clear template defines how income is allocated, how expenses are categorized, and how savings goals are measured.

In 2026, an effective monthly budget template must be digital, flexible, and inflation-aware.

Essential Budget Categories

Every monthly budget template should separate income and expenses into clearly defined categories. Budgeting tips 2026 recommend organizing finances into the following core groups:

1. Income

- Salary or wages

- Business or freelance income

- Passive income streams

- Bonuses or commissions

2. Fixed Expenses

- Rent or mortgage

- Utilities

- Insurance

- Loan payments

3. Variable Expenses

- Groceries

- Transportation

- Dining

- Entertainment

4. Recurring Digital Subscriptions

- Streaming services

- Software memberships

- Online platforms

5. Savings & Investments

- Emergency fund

- Retirement contributions

- Investment accounts

- Short-term goals

Separating subscriptions from general discretionary spending improves visibility and prevents unnoticed cost accumulation.

Recommended Percentage Allocation Guide

While allocations vary by income level, a structured template can follow this reference model:

| Category | Recommended Range | Notes |

|---|---|---|

| Needs (Fixed + Essentials) | 45–55% | Housing should ideally stay under 30% |

| Wants (Lifestyle + Subscriptions) | 20–30% | Review quarterly |

| Savings & Investments | 20–30% | Increase when income rises |

| Debt Repayment (if applicable) | Variable | Prioritize high-interest debt |

This model supports balanced financial growth while aligning with practical budgeting tips 2026.

Fixed vs Variable Expense Structuring

Separating fixed and variable expenses improves forecasting accuracy.

- Fixed expenses remain consistent each month.

- Variable expenses fluctuate and require closer monitoring.

Budgeting tips 2026 emphasize adjusting variable spending first during economic pressure rather than disrupting savings allocations.

Digital vs Spreadsheet Templates

There are two primary formats for implementing a monthly budget template:

Digital Budgeting Apps

- Automatic transaction syncing

- Real-time updates

- Built-in categorization

- Savings tracking dashboards

Spreadsheet-Based Templates

- Full customization

- Manual control

- Clear visual structure

- Offline accessibility

Digital systems reduce errors and improve efficiency, while spreadsheets offer deeper customization. Many individuals combine both for maximum clarity.

AI-Integrated Budget Sheets

Modern budgeting templates increasingly integrate predictive analytics. These systems estimate end-of-month balances based on spending patterns and recurring payments.

Advanced templates can:

- Forecast cash flow gaps

- Highlight category overspending

- Adjust projections based on income changes

- Visualize long-term savings growth

This level of insight supports forward-looking budgeting rather than simple expense recording.

Sample Monthly Budget Layout

| Category | Budgeted Amount | Actual Spending | Difference |

|---|---|---|---|

| Income | $5,000 | $5,000 | — |

| Fixed Expenses | $2,200 | $2,180 | +$20 |

| Variable Expenses | $1,200 | $1,350 | -$150 |

| Subscriptions | $200 | $220 | -$20 |

| Savings | $1,000 | $1,000 | — |

Tracking the “difference” column allows quick identification of overspending or surplus funds.

Summary

A well-designed monthly budget template provides clarity, structure, and accountability. By organizing categories properly, reviewing allocations regularly, and integrating digital tracking, households can apply budgeting tips 2026 consistently and maintain stronger financial control.

Common Budgeting Mistakes to Avoid in 2026

Even with strong budgeting tips 2026 in place, certain mistakes can weaken financial stability. Modern budgeting requires consistency, review, and system-based management. Avoiding common errors improves long-term results and prevents unnecessary financial stress.

Overestimating Income

One of the most frequent budgeting errors is planning expenses around projected income rather than confirmed earnings. This is especially risky for freelancers, commission-based earners, and business owners.

Safer budgeting tips 2026 recommend:

- Basing budgets on average income from the last 3–6 months

- Allocating bonuses separately

- Avoiding commitments tied to uncertain revenue

Conservative income estimation protects against shortfalls.

Ignoring Small Recurring Charges

Micro-subscriptions and digital services often go unnoticed. Individually small, these recurring expenses can significantly impact annual savings.

Common overlooked charges include:

- Streaming services

- App memberships

- Cloud storage plans

- Automatic renewals

Budgeting tips 2026 emphasize conducting quarterly subscription audits to eliminate unnecessary recurring costs.

Relying Entirely on Manual Tracking

Manual tracking increases the risk of missed transactions, delayed updates, and miscalculations. In a digital economy with frequent transactions, spreadsheets alone may not provide sufficient visibility.

Modern budgeting systems benefit from:

- Automatic transaction syncing

- Real-time categorization

- Spending alerts

- Automated savings transfers

System-based tracking reduces human error and improves financial awareness.

Failing to Adjust for Inflation

Inflation gradually reduces purchasing power. A budget that remains unchanged for multiple years may become unrealistic.

Effective budgeting tips 2026 include:

- Reviewing expense allocations quarterly

- Increasing savings rates when income grows

- Adjusting discretionary spending during inflation spikes

Regular adjustments maintain financial balance despite economic changes.

Neglecting Emergency Fund Maintenance

Building an emergency fund is essential, but maintaining it is equally important. Many individuals stop contributing once a basic target is reached.

Financial stability improves when:

- Emergency funds cover 3–6 months of essential expenses

- Contributions continue after withdrawals

- Funds are stored in accessible but separate accounts

A maintained emergency buffer reduces reliance on high-interest debt during unexpected events.

Mixing Needs and Wants Without Clear Categories

Blurring the line between essential and discretionary spending reduces clarity. When categories are unclear, overspending becomes harder to identify.

Budgeting tips 2026 recommend clearly separating:

- Fixed essential costs

- Variable necessities

- Lifestyle expenses

- Savings contributions

Clear categorization improves accountability and decision-making.

Avoiding these common mistakes strengthens the effectiveness of budgeting tips 2026. Structured planning, regular reviews, and automation-based systems create financial resilience and long-term sustainability.

Advanced Smart Budgeting Strategies for 2026

As financial systems become more digital and data-driven, advanced budgeting tips 2026 go beyond basic expense tracking. These strategies focus on forecasting, wealth monitoring, income diversification, and behavioral optimization. They are designed for individuals who want not only stability, but measurable financial growth.

Cash Flow Forecasting

Cash flow forecasting estimates future income and expenses based on historical patterns and recurring obligations. Instead of reacting to shortages, forecasting identifies potential gaps before they occur.

An advanced budgeting system should project:

- Expected income for the next 30–90 days

- Fixed recurring expenses

- Variable spending trends

- Upcoming annual or irregular bills

| Forecast Period | Expected Income | Projected Expenses | Surplus / Shortfall |

|---|---|---|---|

| 30 Days | $5,000 | $4,300 | +$700 |

| 60 Days | $10,000 | $8,900 | +$1,100 |

| 90 Days | $15,000 | $13,800 | +$1,200 |

Budgeting tips 2026 increasingly emphasize forward-looking projections rather than end-of-month summaries.

Net Worth Tracking

Net worth tracking provides a broader financial picture than monthly budgeting alone. Net worth equals total assets minus total liabilities.

Assets may include:

- Cash and savings

- Investment accounts

- Property value

- Retirement funds

Liabilities may include:

- Credit card balances

- Personal loans

- Mortgages

- Student loans

Monitoring net worth quarterly helps measure long-term progress and aligns daily budgeting decisions with wealth-building goals.

Multi-Account Money Management Strategy

Separating funds across multiple accounts improves financial clarity and reduces overspending. Advanced budgeting tips 2026 often recommend structured account segmentation such as:

- Primary spending account

- Bills-only account

- Emergency savings account

- Investment account

- Short-term goal account

This structure limits accidental spending of reserved funds and strengthens automated financial control.

Behavioral Finance Optimization

Financial decisions are influenced by habits and psychology. Advanced budgeting strategies address behavioral triggers that lead to overspending.

Practical behavioral improvements include:

- Implementing 24-hour purchase delays for non-essential items

- Setting predefined spending caps

- Turning off one-click purchase features

- Scheduling fixed “review days” each month

By designing financial systems that reduce impulse decisions, individuals strengthen the effectiveness of budgeting tips 2026.

Strategic Debt Acceleration

Beyond minimum payments, advanced strategies focus on structured debt reduction methods such as:

- Avalanche method (highest interest rate first)

- Snowball method (smallest balance first)

Accelerating debt repayment improves cash flow flexibility and reduces long-term interest costs.

Increasing the Savings Rate Gradually

Instead of making drastic changes, incremental increases in savings contributions improve sustainability.

For example:

| Income Increase | Suggested Savings Increase |

|---|---|

| +5% income | Increase savings by 2% |

| +10% income | Increase savings by 4–5% |

| Bonus received | Allocate 50% to savings |

Gradual increases prevent lifestyle inflation while strengthening long-term financial growth.

Advanced budgeting tips 2026 focus on forecasting, wealth measurement, structured account systems, behavioral discipline, and strategic debt management. When combined with automation and real-time tracking, these strategies create a comprehensive financial framework designed for stability and long-term wealth accumulation.

Conclusion

Smart financial management in today’s economy requires more than tracking expenses. The most effective budgeting tips 2026 emphasize automation, structured allocation methods, inflation awareness, subscription monitoring, and long-term wealth tracking. Modern budgeting is proactive, system-based, and digitally supported.

By combining automated savings, real-time expense visibility, structured frameworks such as zero-based budgeting or the 50/30/20 rule, and advanced strategies like cash flow forecasting and net worth tracking, individuals can build a resilient financial structure. Consistency, periodic review, and gradual savings increases remain essential for sustainable growth.

When applied correctly, budgeting tips 2026 help protect purchasing power, reduce debt dependency, and strengthen long-term financial stability in an increasingly digital and subscription-driven economy.

Frequently Asked Questions (FAQs)

1. What are the most important budgeting tips 2026?

The most important budgeting tips 2026 include automating savings, tracking expenses in real time, adjusting budgets for inflation, building a 3–6 month emergency fund, and using structured frameworks like zero-based budgeting or the 50/30/20 rule.

2. Which budgeting method works best in 2026?

The best method depends on income stability and financial goals. Zero-based budgeting offers detailed control and works well for aggressive savings or variable income. The 50/30/20 rule provides simplicity and is effective for stable, predictable earnings.

3. How much should I save each month in 2026?

A common benchmark is saving at least 20% of after-tax income. However, savings rates may increase during higher-income periods or decrease temporarily during economic strain. Consistency and gradual increases are more important than short-term spikes.

4. How do I automate my savings effectively?

Automation can be implemented through payroll deposit splitting, scheduled bank transfers, percentage-based allocations, and round-up savings programs. Setting transfers to occur immediately after payday improves consistency.

5. Are budgeting apps necessary in 2026?

While not mandatory, digital budgeting tools significantly improve accuracy and efficiency. They help track subscriptions, categorize expenses automatically, and provide real-time financial visibility, which supports the practical application of budgeting tips 2026.

6. How often should I review my budget?

Budgets should be reviewed monthly and adjusted quarterly. Major life events, income changes, or inflation spikes may require immediate revisions.

7. What is the ideal emergency fund amount?

An emergency fund should cover three to six months of essential living expenses. This buffer reduces reliance on credit and provides financial security during unexpected events.

Disclaimer

The information on this website is provided for general informational and educational purposes only. We are not licensed financial advisors, accountants, attorneys, or investment professionals, and our content does not constitute financial, legal, tax, or investment advice.

Any actions you take based on the information on this website are at your own risk. Financial decisions involve risk, and you should consult a qualified professional before making any financial choices.

While we aim to provide accurate and up-to-date information, we make no guarantees regarding completeness or reliability. We are not responsible for any losses, damages, or outcomes resulting from the use of our content or third-party links.