AI tools for personal finance 2026 are reshaping how individuals budget, invest, and plan taxes through automation, predictive analytics, and machine learning models. Modern AI budgeting apps categorize expenses in real time, robo-advisors 2026 platforms rebalance portfolios algorithmically, and AI investment platforms analyze market data at scale.

The expansion of automated financial planning reflects broader fintech trends, including personalized dashboards, behavioral modeling, and AI-driven tax optimization. However, not all AI tools for personal finance deliver equal value. Differences in transparency, regulatory oversight, algorithm design, and fee structures can significantly impact outcomes.

Financial regulators such as the U.S. Securities and Exchange Commission and the Financial Industry Regulatory Authority continue emphasizing investor protection, disclosure standards, and fiduciary responsibility as AI adoption accelerates. Platforms operating without clear compliance frameworks may expose users to avoidable risks.

This guide evaluates which AI tools for personal finance 2026 are worth using, which require caution, and which to avoid entirely. The focus is on measurable performance factors, cost transparency, algorithm accountability, and data security—not marketing claims.

Summary

AI tools for personal finance 2026 automate budgeting, investing, and tax planning using machine learning and predictive models. While they reduce costs and improve efficiency, careful evaluation of regulation, fees, and transparency is essential before adoption.

Key Takeaways

- AI tools for personal finance 2026 integrate budgeting, investing, and tax automation.

- AI budgeting apps prioritize real-time expense categorization and forecasting.

- Robo-advisors 2026 use algorithmic portfolio rebalancing and tax-loss harvesting.

- AI investment platforms vary in risk exposure and transparency.

- Automated financial planning enhances efficiency but does not remove market risk.

What Are AI Tools for Personal Finance?

AI tools for personal finance are software platforms that use machine learning, predictive analytics, and automation to manage budgeting, investing, saving, and tax planning. In 2026, AI tools for personal finance analyze real-time financial data, detect patterns, and generate recommendations without continuous manual input.

These systems power AI budgeting apps, robo-advisors 2026 platforms, and AI investment platforms. Unlike traditional financial software that relies on fixed rules, AI-driven systems adapt based on user behavior, spending history, market movements, and risk tolerance.

How Artificial Intelligence Is Used in Finance

AI in personal finance typically performs five core functions:

- Data aggregation – Consolidates bank accounts, credit cards, loans, and investments.

- Pattern recognition – Identifies recurring expenses and spending anomalies.

- Predictive forecasting – Estimates future cash flow and savings gaps.

- Automated portfolio management – Rebalances assets based on market shifts.

- Tax optimization – Identifies deductible opportunities and tax-loss harvesting.

Robo-advisors offered by firms such as Betterment and Wealthfront use algorithmic asset allocation models, often based on Modern Portfolio Theory. Some hybrid models from firms like Vanguard combine AI automation with limited human oversight.

Types of AI Financial Tools

| Tool Type | Primary Function | AI Capability | Risk Level | Best For |

|---|---|---|---|---|

| AI Budgeting Apps | Expense tracking | Spending prediction & categorization | Low | Daily money management |

| Robo-Advisors 2026 | Portfolio management | Algorithmic rebalancing | Moderate | Long-term investors |

| AI Investment Platforms | Active strategy execution | Predictive market modeling | High | Risk-tolerant investors |

| Automated Financial Planning | Retirement & tax strategy | Scenario simulation | Moderate | Structured planners |

How AI Differs from Traditional Financial Software

Traditional tools operate on static rules (e.g., fixed budget categories). AI tools for personal finance continuously learn from user inputs and market data. They update recommendations dynamically rather than relying on preset formulas.

However, AI systems can function as “black boxes,” meaning users may not fully understand how decisions are generated. This raises transparency and regulatory concerns, especially in investment management, where oversight from bodies like the U.S. Securities and Exchange Commission plays a critical role.

Summary

AI tools for personal finance use adaptive algorithms to automate budgeting, investing, and tax planning. Unlike traditional software, they continuously learn from data patterns, but they require evaluation for transparency, risk exposure, and regulatory compliance.

Key Takeaways

- AI tools for personal finance automate financial decisions using predictive models.

- AI budgeting apps focus on expense categorization and forecasting.

- Robo-advisors 2026 manage portfolios through algorithmic rebalancing.

- AI investment platforms carry higher volatility and transparency risks.

- Regulatory oversight improves investor protection but does not eliminate risk.

AI Budgeting Apps: Benefits and Limitations

AI budgeting apps are among the most widely adopted AI tools for personal finance in 2026. These platforms automate expense tracking, categorize transactions using machine learning, and forecast cash flow based on historical behavior. Unlike manual spreadsheets, AI budgeting apps adjust dynamically as spending patterns change.

By analyzing transaction data in real time, AI budgeting apps can identify recurring subscriptions, detect unusual charges, and generate automated savings recommendations. Many platforms also provide behavioral nudges designed to improve financial discipline.

How AI Budgeting Apps Work

AI budgeting apps typically operate through three technical layers:

- Data aggregation – Securely connects to bank accounts and credit cards.

- Machine learning categorization – Classifies expenses automatically.

- Predictive forecasting – Projects future balances and savings rates.

Some advanced platforms integrate natural language processing to allow conversational budgeting queries, reflecting broader fintech trends toward AI-driven financial assistants.

Key Features to Look For

When evaluating AI tools for personal finance focused on budgeting, consider measurable features:

- Automated expense categorization accuracy (above 90%)

- Real-time cash flow forecasting

- Subscription detection alerts

- Goal-based savings automation

- Bank-level encryption standards

- Multi-account integration

Benefits of AI Budgeting Apps

- Time efficiency – Reduces manual data entry.

- Spending awareness – Highlights behavioral patterns.

- Cash flow visibility – Improves short-term planning.

- Lower cost – Often free or low subscription fees.

For individuals seeking automated financial planning at a basic level, AI budgeting apps offer structured guidance without requiring investment management complexity.

Limitations and Risks

Despite advantages, AI tools for personal finance in the budgeting category have constraints:

- Data privacy exposure – Requires financial account access.

- Over-categorization errors – Misclassification can distort insights.

- Limited strategic advice – Budgeting ≠ wealth management.

- Behavioral over-reliance – Users may depend on alerts instead of discipline.

Data security oversight varies by provider. Users should verify encryption standards and compliance practices aligned with regulatory frameworks monitored by authorities such as the Financial Industry Regulatory Authority.

Who Should Avoid AI Budgeting Apps?

AI budgeting apps may not be ideal for:

- Individuals uncomfortable linking bank accounts

- Users requiring complex tax strategy integration

- Investors seeking portfolio-level optimization

- High-net-worth individuals needing fiduciary oversight

Summary

AI budgeting apps are entry-level AI tools for personal finance that automate expense tracking and forecasting. They improve efficiency and visibility but do not replace comprehensive financial planning or investment advisory services.

Key Takeaways

- AI budgeting apps automate expense categorization and forecasting.

- They are low-cost and suitable for daily financial management.

- Data privacy and categorization errors remain key risks.

- They support—but do not replace—automated financial planning systems.

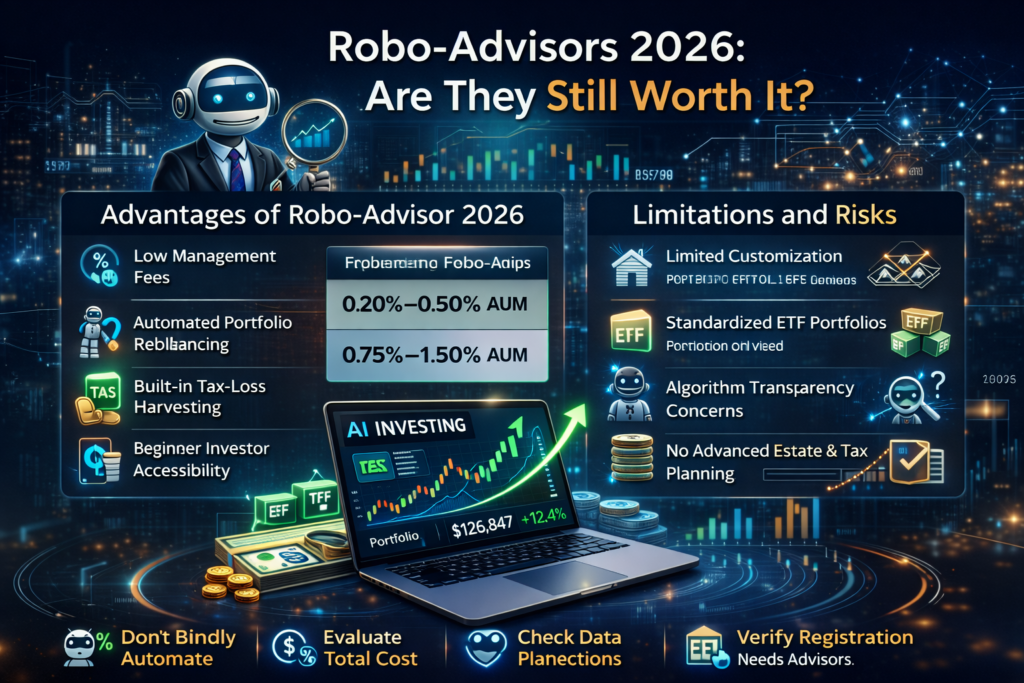

Robo-Advisors 2026: Are They Still Worth It?

Robo-advisors 2026 remain a central category within AI tools for personal finance, offering automated portfolio construction, rebalancing, and tax optimization at lower fees than traditional advisors. These platforms use algorithm-driven asset allocation models to match portfolios with an investor’s risk tolerance, time horizon, and financial goals.

As automated financial planning becomes more mainstream, robo-advisors 2026 increasingly combine artificial intelligence with behavioral analytics and real-time market data to adjust allocations dynamically.

How Robo-Advisors Use Algorithms

Most robo-advisors follow a structured process:

- Risk profiling questionnaire

- Algorithmic asset allocation (often ETF-based portfolios)

- Automated rebalancing

- Tax-loss harvesting (where applicable)

Platforms such as Betterment and Wealthfront use diversified ETF portfolios aligned with Modern Portfolio Theory principles. Hybrid models from firms like Vanguard integrate automated portfolio management with optional human advisor access.

Fees Compared to Human Advisors

| Feature | Robo-Advisor | Human Financial Advisor |

|---|---|---|

| Management Fees | 0.20%–0.50% AUM | 0.75%–1.50% AUM |

| Portfolio Rebalancing | Automated | Manual or semi-automated |

| Tax-Loss Harvesting | Often included | May cost extra |

| Personalization Depth | Algorithm-based | Highly customized |

| Minimum Investment | Often low or none | Typically higher |

Lower fees make robo-advisors 2026 attractive for cost-sensitive investors. However, personalization and complex planning remain limited compared to fiduciary advisory services.

Performance and Market Volatility

A common question is whether robo-advisors outperform the market. In most cases, they aim to track diversified index strategies rather than beat benchmarks. Returns largely depend on asset allocation rather than algorithm “intelligence.”

During volatile markets, automated rebalancing can maintain discipline. However, algorithms may not account for nuanced economic signals beyond pre-programmed thresholds.

Regulatory oversight from bodies such as the U.S. Securities and Exchange Commission helps ensure disclosure standards, but performance guarantees do not exist.

Advantages of Robo-Advisors 2026

- Low management fees

- Automated portfolio rebalancing

- Built-in tax-loss harvesting

- Accessibility for beginner investors

- Reduced emotional investing

Limitations and Risks

- Limited customization for complex financial situations

- Standardized ETF portfolios

- Algorithm transparency concerns

- No holistic estate or advanced tax planning

Summary

Robo-advisors 2026 are cost-efficient AI tools for personal finance that automate portfolio management using algorithmic asset allocation. They suit long-term investors seeking disciplined, diversified strategies but may not replace comprehensive human advisory services.

Key Takeaways

- Robo-advisors 2026 provide automated investing at lower fees.

- Performance typically tracks diversified index strategies.

- AI tools for personal finance in this category reduce emotional bias.

- Complex financial needs may require human oversight.

AI Investment Platforms: Smarter Returns or Higher Risk?

AI investment platforms represent the most aggressive segment of AI tools for personal finance in 2026. Unlike robo-advisors 2026 that primarily focus on diversified ETF portfolios, AI investment platforms often attempt predictive stock selection, sentiment analysis, and algorithmic trade execution.

These systems rely on large-scale data modeling, including price history, earnings reports, macroeconomic indicators, and alternative data sources. While marketed as advanced AI tools for personal finance, their risk profile is typically higher than automated financial planning or passive robo-advisory solutions.

Predictive Models and Machine Learning

AI investment platforms commonly use:

- Supervised machine learning models trained on historical market data

- Natural language processing (NLP) to analyze earnings calls and news sentiment

- Quantitative factor modeling (momentum, value, volatility signals)

- Automated trade execution systems

Some platforms incorporate generative AI technologies influenced by developments from organizations such as OpenAI to enhance data interpretation interfaces. However, interface intelligence does not guarantee superior investment outcomes.

AI-Driven Stock Picking vs Index Investing

| Strategy Type | Risk Level | Cost | Transparency | Long-Term Evidence |

|---|---|---|---|---|

| AI Stock Picking | High | Moderate–High | Often Limited | Mixed |

| Index ETF Investing | Moderate | Low | High | Strong historical data |

Research consistently shows that long-term passive index strategies outperform most active management strategies after fees. AI investment platforms attempting short-term alpha generation must overcome transaction costs, slippage, and market efficiency constraints.

Transparency and “Black Box” Algorithms

One major concern with AI tools for personal finance in this category is algorithm opacity. Many AI investment platforms do not disclose:

- Model architecture

- Training data sources

- Risk exposure thresholds

- Stress-testing methodology

This creates evaluation challenges for retail investors. Without transparency, risk cannot be fully assessed.

Regulatory Oversight and Investor Protection

AI investment platforms operating in the United States must comply with regulations monitored by the U.S. Securities and Exchange Commission and brokerage standards enforced by the Financial Industry Regulatory Authority.

However, compliance does not eliminate:

- Market volatility risk

- Model overfitting risk

- Liquidity risk

- Execution timing risk

Advantages of AI Investment Platforms

- Advanced data analysis at scale

- Faster execution than manual trading

- Potential short-term opportunity detection

- Integration with automated financial planning dashboards

Risks and Limitations

- Higher volatility exposure

- Performance inconsistency

- Algorithmic overfitting

- Increased transaction costs

- Limited explainability

Summary

AI investment platforms are high-complexity AI tools for personal finance designed for predictive trading and active strategy execution. While technologically advanced, they carry significantly higher risk compared to passive robo-advisors 2026 models.

Key Takeaways

- AI investment platforms attempt predictive market strategies.

- Risk levels are higher than traditional robo-advisors.

- Transparency varies significantly between providers.

- Long-term index investing remains evidence-supported.

- Not all AI tools for personal finance are equally suitable for risk-averse investors.

Automated Financial Planning and Tax Tools

Automated financial planning platforms expand AI tools for personal finance beyond budgeting and investing into retirement modeling, tax optimization, and long-term wealth projections. In 2026, these systems use machine learning and scenario simulation to forecast savings gaps, withdrawal strategies, and tax liabilities.

Unlike basic AI budgeting apps, automated financial planning tools integrate multiple financial variables—income growth, inflation, asset allocation, and tax brackets—into dynamic projections. This reflects broader fintech trends toward fully integrated financial dashboards.

AI in Retirement Planning

AI-powered retirement modules typically provide:

- Monte Carlo simulations to estimate probability of retirement success

- Dynamic withdrawal modeling based on market conditions

- Inflation-adjusted forecasting

- Social Security optimization scenarios

These features allow users to stress-test long-term strategies under different market conditions. However, projections are probability-based—not guarantees.

AI Tax Optimization Tools

Tax-focused AI tools for personal finance analyze transaction data to identify:

- Tax-loss harvesting opportunities

- Deduction eligibility patterns

- Capital gains timing strategies

- Estimated quarterly tax calculations

Some platforms align calculations with guidelines issued by the Internal Revenue Service, helping users reduce filing errors. However, automated tools cannot fully replace a certified tax professional in complex cases involving business income, international assets, or estate structures.

Accuracy vs Human CPA Review

| Feature | AI Tax Tool | Certified Public Accountant |

|---|---|---|

| Speed | Instant analysis | Slower review process |

| Cost | Low subscription | Higher service fees |

| Complex Case Handling | Limited | Advanced |

| Real-Time Monitoring | Yes | No |

| Legal Representation | No | Yes |

AI-powered automated financial planning improves efficiency, especially for salaried individuals with straightforward finances. Yet edge cases—such as multi-state taxation, inheritance planning, or corporate equity compensation—require human expertise.

Advantages of Automated Financial Planning

- Scenario-based long-term forecasting

- Integrated budgeting, investing, and tax data

- Faster calculations and updates

- Lower cost compared to full-service advisory firms

Limitations and Risks

- Overconfidence in probability projections

- Limited personalization for complex estates

- Dependence on accurate data inputs

- Regulatory interpretation limitations

Summary

Automated financial planning tools extend AI tools for personal finance into retirement and tax optimization. They provide scenario modeling and efficiency but cannot fully replace professional financial or tax advisors in complex situations.

Key Takeaways

- Automated financial planning integrates retirement and tax modeling.

- AI tax tools improve efficiency but have structural limits.

- Compliance alignment with tax authorities enhances accuracy.

- Complex financial cases still require human oversight.

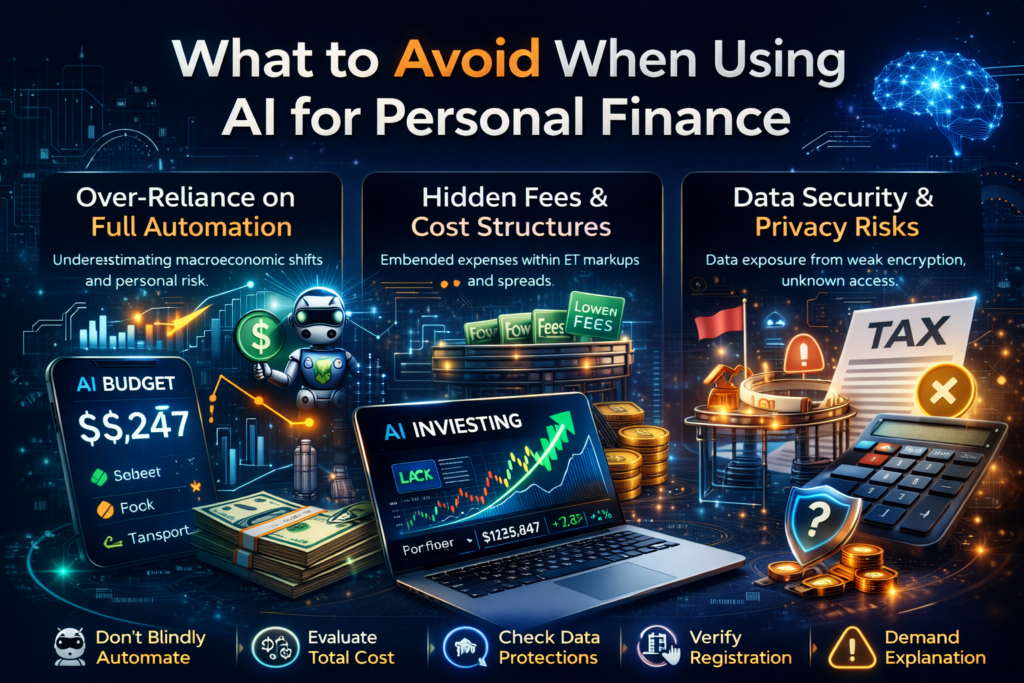

What to Avoid When Using AI for Personal Finance

Not all AI tools for personal finance deliver measurable value. While automation improves efficiency, certain risks increase when users rely on opaque systems without evaluating cost structures, compliance standards, or algorithm design. In 2026, responsible adoption requires understanding where automation should stop.

Over-Reliance on Full Automation

AI tools for personal finance are designed to assist decision-making—not replace judgment. Over-automation can lead to:

- Blind acceptance of investment allocations

- Ignoring macroeconomic shifts

- Failure to reassess risk tolerance

- Reduced financial literacy over time

Even robo-advisors 2026 models operate within predefined asset allocation logic. They cannot anticipate personal life events such as job loss, health emergencies, or inheritance changes unless manually updated.

Hidden Fees and Cost Structures

Some AI investment platforms promote low advisory fees while incorporating:

- ETF expense ratios

- Spread markups

- Transaction costs

- Premium feature subscriptions

A platform advertising 0.25% AUM may carry higher effective costs once embedded fund expenses are included. Transparent fee disclosure is a critical evaluation factor for AI tools for personal finance.

Data Security and Privacy Risks

AI budgeting apps and automated financial planning systems require access to sensitive financial data. Risks include:

- Third-party data sharing

- Inadequate encryption

- API vulnerabilities

- Credential storage exposure

Investors should verify compliance standards and brokerage protections monitored by organizations such as the Financial Industry Regulatory Authority. However, regulatory oversight reduces—but does not eliminate—cybersecurity risk.

Unregulated or Offshore Platforms

AI investment platforms operating without proper registration may lack oversight from authorities such as the U.S. Securities and Exchange Commission. Warning signs include:

- No clear regulatory registration number

- Guaranteed return claims

- Vague algorithm explanations

- Aggressive performance marketing

Financial markets inherently involve risk. Any AI tools for personal finance promising consistent outperformance without volatility exposure warrant caution.

Algorithmic Transparency Concerns

“Black box” AI models create accountability gaps. If a portfolio allocation shifts significantly, users should be able to identify:

- What triggered the change

- Risk exposure adjustments

- Rebalancing thresholds

- Downside protection logic

Without transparency, performance evaluation becomes difficult.

Summary

When using AI tools for personal finance, avoid over-reliance on automation, hidden fee structures, weak data protection, and unregulated providers. Transparency, regulatory compliance, and cost clarity are essential safeguards.

Key Takeaways

- Automation does not remove financial risk.

- Hidden fees can reduce long-term returns.

- Data security must be verified before linking accounts.

- Regulatory oversight improves protection but does not guarantee outcomes.

- Guaranteed-return claims are a major red flag.

How to Choose the Right AI Financial Tool

Choosing the right AI tools for personal finance in 2026 requires structured evaluation. Not all platforms serve the same purpose. AI budgeting apps focus on expense control, robo-advisors 2026 prioritize diversified portfolio automation, and AI investment platforms target active market strategies. Selection should align with financial complexity, risk tolerance, cost sensitivity, and long-term planning priorities — including clearly defined financial goals for Millennials and Gen Z.

Step 1: Define Your Primary Financial Goal

Start by identifying your core objective:

- Daily expense control → AI budgeting apps

- Long-term passive investing → Robo-advisors 2026

- Active strategy experimentation → AI investment platforms

- Retirement and tax modeling → Automated financial planning

Misalignment between tool type and financial goal increases risk.

For example, individuals focused on early-stage wealth building, debt reduction, or retirement acceleration should align their tool selection with structured financial planning frameworks. This is particularly important when mapping AI adoption to broader financial goals for millennials and Gen Z , where life stage significantly influences budgeting, investing, and risk decisions.

Step 2: Assess Risk Tolerance

AI tools for personal finance vary in volatility exposure.

| User Risk Profile | Suitable Tool | Risk Level |

|---|---|---|

| Conservative | Robo-advisor (ETF-based) | Moderate |

| Moderate | Automated financial planning + robo-advisor | Moderate |

| Aggressive | AI investment platform | High |

| Budget-Focused | AI budgeting app | Low |

Higher algorithmic complexity often correlates with higher volatility.

Step 3: Evaluate Fee Structure

Look beyond advertised management fees. Total cost includes:

- Advisory percentage (AUM)

- ETF expense ratios

- Subscription costs

- Trading spreads

- Premium feature upgrades

Transparent AI tools for personal finance clearly disclose total effective annual cost.

Step 4: Verify Regulation and Compliance

Before linking financial accounts, confirm:

- Registration with the U.S. Securities and Exchange Commission (if investment-related)

- Brokerage compliance standards monitored by the Financial Industry Regulatory Authority

- Clear privacy and encryption disclosures

- No guaranteed-return claims

Regulatory alignment reduces fraud risk but does not eliminate market risk.

Step 5: Demand Algorithm Transparency

Users should understand:

- How portfolios are constructed

- Rebalancing frequency

- Risk exposure thresholds

- Tax optimization triggers

Opaque “black box” systems limit informed oversight.

Decision Framework

| Financial Need | Recommended Tool | Avoid |

|---|---|---|

| Basic budgeting | AI budgeting app | High-fee investment platform |

| Passive long-term growth | Robo-advisor 2026 | Day-trading AI system |

| Tax efficiency | Automated financial planning tool | Non-compliant offshore platform |

| Speculative trading | AI investment platform (regulated) | Guaranteed-return AI schemes |

Summary

Selecting AI tools for personal finance requires aligning tool type with goals, risk tolerance, cost transparency, and regulatory oversight. Clear disclosure, fee visibility, algorithm transparency, and alignment with generational financial planning priorities are essential evaluation criteria.

Key Takeaways

- Match the tool to your financial objective.

- Align AI adoption with clearly defined financial goals.

- Evaluate total cost—not just advertised fees.

- Confirm regulatory compliance before investing.

- Higher automation does not mean lower risk.

- Transparency is a non-negotiable requirement in 2026.

Conclusion

AI tools for personal finance in 2026 offer measurable advantages in automation, cost efficiency, and real-time financial analysis. AI budgeting apps improve expense control, robo-advisors 2026 streamline diversified investing, and AI investment platforms expand access to data-driven strategies. Automated financial planning systems further integrate retirement modeling and tax optimization.

However, AI tools for personal finance do not eliminate market risk, behavioral bias, or structural volatility. Performance depends on asset allocation, fee control, regulatory oversight, and responsible usage. Transparent cost structures, compliance verification, and algorithm clarity remain essential evaluation criteria.

Adoption should be intentional, not trend-driven. In 2026, the most effective use of AI tools for personal finance combines automation with informed oversight and disciplined financial planning.

Frequently Asked Questions (FAQs)

1. Are AI tools for personal finance safe?

AI tools for personal finance are generally safe when offered by regulated providers that comply with oversight from the U.S. Securities and Exchange Commission and brokerage standards monitored by the Financial Industry Regulatory Authority. However, market risk, cybersecurity exposure, and algorithm limitations still apply.

2. What is the best AI budgeting app in 2026?

The best AI budgeting apps prioritize accurate expense categorization, real-time forecasting, subscription detection, transparent pricing, and strong encryption standards. Selection depends on financial objectives, integration needs, and cost sensitivity rather than brand popularity.

3. Do robo-advisors outperform the market?

Most robo-advisors 2026 platforms aim to track diversified index strategies rather than outperform benchmarks. Long-term returns typically depend on asset allocation, diversification, and fee efficiency rather than algorithmic market timing.

4. Can AI replace human financial advisors?

AI tools for personal finance can automate portfolio management, rebalancing, and financial forecasting. However, they do not fully replace human advisors in complex cases involving estate planning, advanced tax structuring, business ownership, or behavioral financial coaching.

5. Are AI investment platforms regulated?

AI investment platforms operating in the United States must register with the U.S. Securities and Exchange Commission and comply with brokerage regulations enforced by the Financial Industry Regulatory Authority. Investors should verify registration before committing capital.

6. Is automated financial planning accurate?

Automated financial planning tools use probability modeling and historical assumptions to project outcomes. While effective for structured forecasting, projections are scenario-based and cannot guarantee future financial performance.

Disclaimer

The information on this website is for educational and informational purposes only. I am not a licensed financial advisor, accountant, or investment professional, and the content should not be considered financial advice.

All decisions regarding investments, debt, taxes, or financial planning should be made based on your personal circumstances and, when appropriate, in consultation with a qualified professional. I do not guarantee the accuracy or completeness of the information provided, and you are responsible for your own financial decisions.